A Family Business at a Bargain Price

4.5x earnings. 0.49x book value.

Key Metrics:

30+ years of dividends.

Consistently profitable since 2007.

5 back-to-back years of record revenue.

4.5x earnings.

0.49x book value.

In the 1880s, a young Thomas F. Braime was an apprentice at an engineering company in Hunslet, building steam traction engines.

One day, the machine got the better of him, and he lost his thumb.

Ambitious by nature, and if anything more determined after the accident, he started looking for better ways to apply oil to machinery.

The answer he came up with was pressed steel oilcans.

In 1888, he rented a small building in Hunslet and set up production.

The cans were good. They sold well and quickly built a reputation for quality. As the new motor industry started to grow, demand for his pressed metal grew along with it.

By the early 1910s the original workshop wasn’t big enough anymore, and larger premises were needed to support the first serious expansion.

So a large factory was built on Hunslet Road between 1911 and 1914.

Braime Group PLC

Ticker: BMT / BMTO | Market cap: £15.6 million

The family still runs the business out of that same building today, more than a century later.

For a long time, the company was basically just the pressings business. The real turning point, at least for understanding the company you can buy today, came in 1971, when they set up the “4B” division to serve the bucket elevator and conveyor market.

Then in 1984 they added an electronics range to 4B and opened their first international office, just outside Chicago.

And from there, the international expansion never really stopped.

They opened subsidiaries in France in 1991, then Thailand in 2003, Germany in 2005, South Africa in 2008, Australia in 2010, China in 2018, the UAE in 2023, Indonesia in 2024, and Canada in 2025.

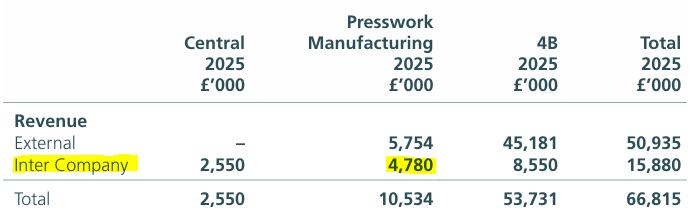

Today the 4B division makes up 89% of sales. It produces and sells everything you need to move and monitor bulk materials safely and efficiently.

Things like elevator buckets, belts, chains, sensors, monitoring software, and other components.

Their customers range from farmers and silo operators to ports and cement plants, basically anyone who moves heavy stuff.

The original Braime pressings segment is still around, though much smaller now at 11% of revenue.

They still make precision metal pressings, mostly for the automotive and construction industries.

And even though the two segments sound pretty different, they’re more connected than you’d think. Almost half of what Braime Pressings produces is sold internally, like bolts and steel buckets that feed straight back into the 4B division.

So even though Pressings looks fairly small and unimportant from the outside, it’s strategically useful, and management says as much:

“The board believes the business continues to add strategic value through its supply to the 4B division and complementary engineering expertise.” – 2025 annual report

The Numbers

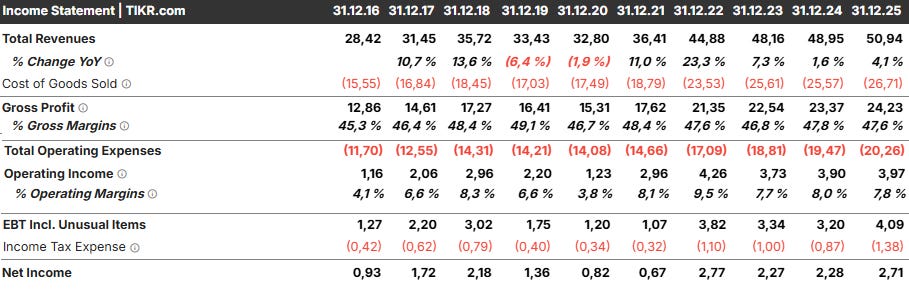

Aside from a small dip in 2019 and 2020, revenue has grown pretty consistently for the past decade.

The last five years have been particularly good. Every single year from 2021 through 2025 set a new revenue record.

Gross profit has moved roughly in line with revenue, and operating profit looks a touch better, because margins have slightly improved over a ten-year window.

One thing I really want to highlight is the consistency here.

Braime has been profitable every single year since 2007. And they’ve paid a dividend every year for 34 years, with the only real gap being the years leading up to the financial crisis.

It’s not a huge dividend, at 16.50p per share for 2025, that works out to a yield of 1.9%, but they’ve raised it gently every year.

I think that kind of consistency says a lot, especially for a company this small.

Another thing I want to touch on, because I think it matters for understanding this business, is how their revenue is actually built up.

Especially when it comes to geographic diversification.

As you know by now, the 4B division is the backbone of the business.

What you might not know is where that revenue comes from.

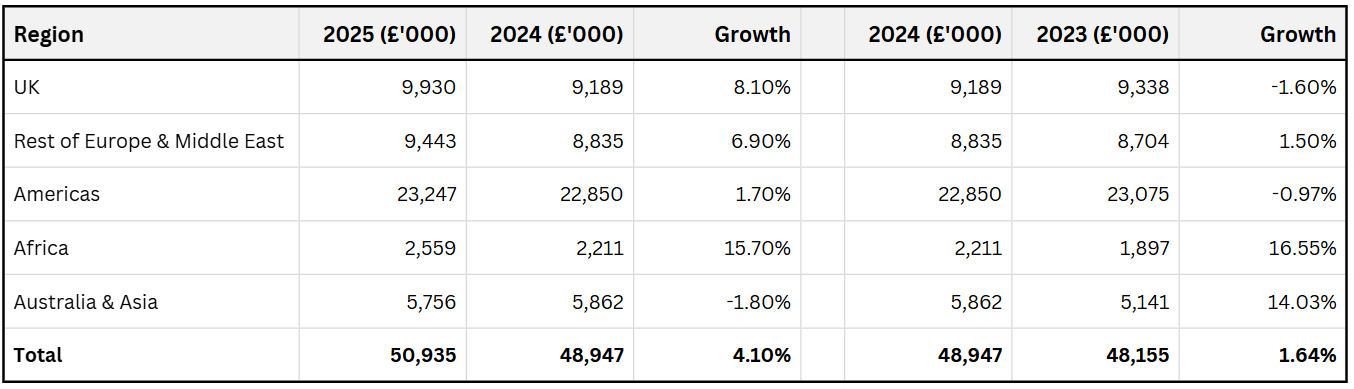

The division has operations in the UK, France, South Africa, Australia, Thailand, Indonesia, Canada, China, the UAE and the United States, which gives the company a nice spread of demand across very different markets.

The positive effect of that becomes clear when we look at the numbers over the past two years.

In 2025, the Australasia region was down 1.8%. But the UK, Europe and the Middle East, the Americas and Africa all grew.

Africa was especially strong with 15.7% growth.

Which allowed the company to record 4.1% overall revenue growth for the year.

In 2024 the story was no different.

Revenue was basically flat in the Americas and Europe, but Africa and Australasia grew 16.6% and 14%, which again delivered a record year with 1.64% total growth.

So in both years, even though some regional markets were stagnant or shrinking, the company still managed to grow in absolute terms.

That shows that their expansion strategy works out quite well and is doing exactly what it’s supposed to.

And they’re still at it. In September 2025 they opened a new subsidiary in Canada to go after the grain market there.

Balance Sheet

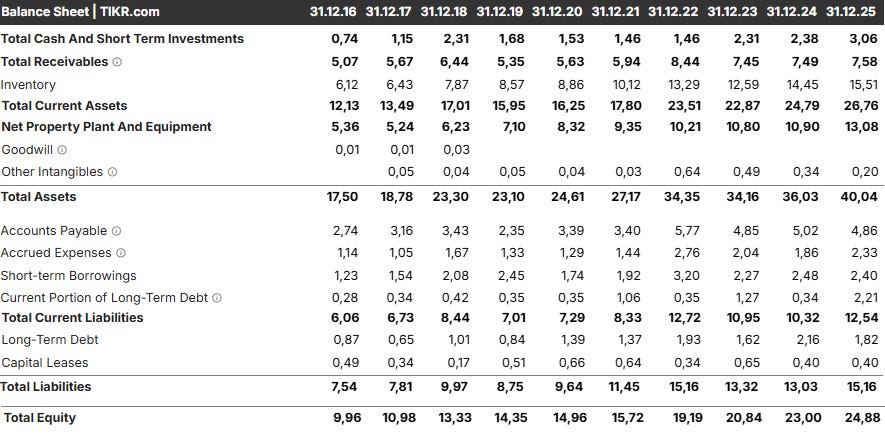

As of 31 December 2025, there isn’t much to complain about on the balance sheet.

They hold a healthy amount of cash, carry little debt, and the whole thing reflects patient and conservative financial management.

Equity has compounded at 11.17% a year over the past decade, and almost all of that came from retained earnings.

The strategy that got them here

Since the 1980s, Braime’s core strategy has been growth through expansion.

But that doesn’t always mean opening a new office.

In 2024 it meant buying four acres of land next to their US warehouse in Illinois. In 2025 it meant opening a subsidiary in Canada. And it meant buying their main supplier for electronic components.

„Our strategy is to invest in increasing our market reach while continuing to develop new products.“

The Acquisition

This is probably the most important thing to have happened to Braime in years, and it’s worth going through properly.

For more than 40 years, a small company called Don Electronics was Braime’s main manufacturing partner for electronic monitoring components.

In plain terms, Don designed and built the electronics that go into the 4B product range.

“Don have been our longstanding partners for over 40 years, responsible for the creation and manufacture of our range of electronic products.”

And as is always the case, whenever Braime bought electronics from Don, they were also paying Don’s profit margin as part of the price.

So on the 31st of March 2026, Braime bought Don Electronics outright, to bring that in-house and keep that margin instead of paying it out.

Don Electronics itself owns 100% of Synatel Instrumentation, a business that specializes in level controls, sensors and safety control systems for hazardous environments, which fits right into the 4B product range.

In the year to 31 March 2025, the two businesses together did £10.6m of revenue and £2.0m of profit before tax. Don did £7.1m of revenue at a 22.5% pre-tax margin, and Synatel did £3.5m at an 11.4% margin. Combined, they had about £6.1m of net assets.

Two solid little businesses. Acquired for strategic reasons.

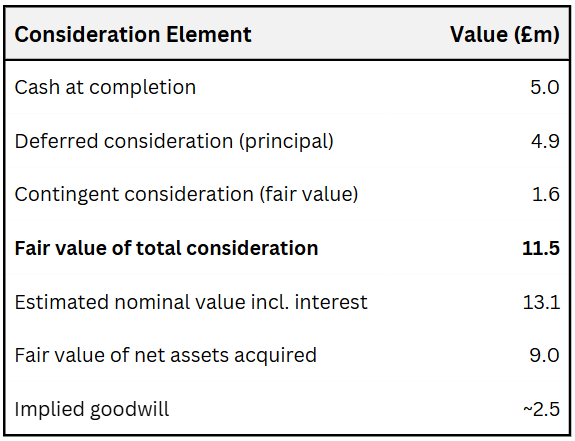

Here’s what Braime paid:

The £5.0m cash payment at completion was funded by a new £5.2m HSBC term loan, with a 41-month initial term to August 2029, amortised over seven years at the BoE base rate plus 2.6%. The £4.9m of deferred consideration gets paid off at £750k a year for three years, with the remaining £2.65m due six months after the third anniversary, accruing interest at base rate plus 3%. The contingent consideration of up to £1.6m is payable in years 4, 5 and 6, but only if the businesses hit certain profit targets.

On the fair value of consideration of about £11.5m against combined pre-tax profit of £2.0m, Braime is paying 5.75x PBT. If you assume a 25% tax rate, that’s 7.7x post-tax earnings.

On book value, £11.5m is 1.9x the £6.1m of combined net assets.

New Structure

The acquisition has a few other implications that I’d like to highlight here.

First, it gives Braime more control over its supply chain and removes a key dependency in the most important part of the business.

“The acquisition of the Group’s principal manufacturer of electronic components brings the supply of this important product under the Group’s control.”

Second, and this ties directly into the first point, it gives Braime control of product development. The company has said again and again that a lot of its recent growth has come from new electronic products, so owning that development process rather than relying on an outside partner is a clear advantage.

„These businesses also further strengthen and enhance the Group’s capabilities to bring new designs to market, in line with the Group’s strategy for continually developing innovative end-user products.“

Third, it captures Don’s margin and keeps it inside the group. This is probably the most important point, so I want to walk through the numbers.

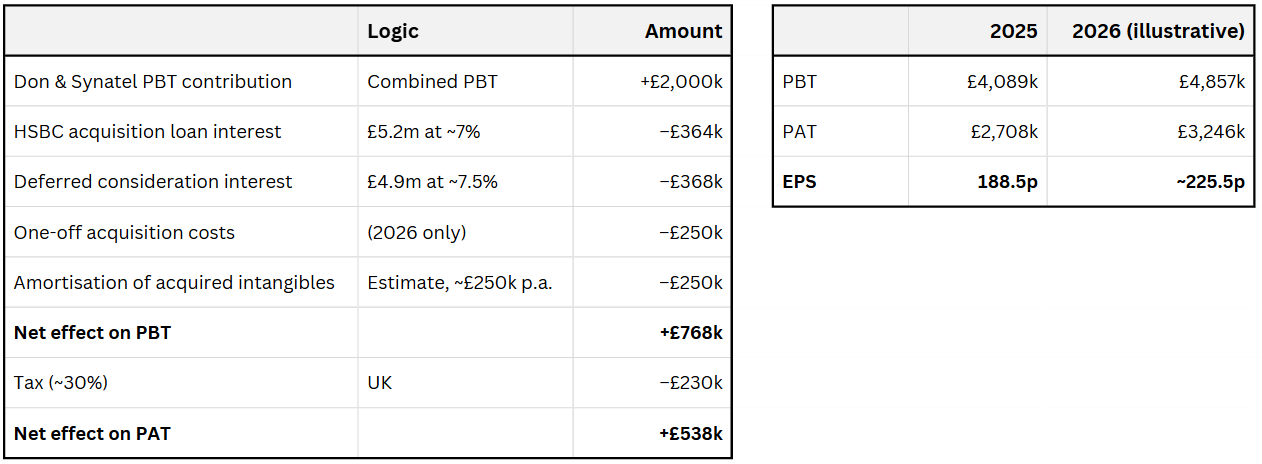

What it could do to earnings

Before the acquisition, Don was selling electronics to 4B at a price that included Don’s 22.5% margin. Then 4B sold those products on to end customers at its own margin on top of that.

After the acquisition, those Don-to-4B sales become internal and get cancelled out on consolidation. What’s left is Braime’s revenue from external customers, and on the cost side, only Don’s actual production cost rather than the marked-up price 4B used to pay. The difference, which is Don’s old margin, now stays inside the group.

The announcement makes this exact point:

“This acquisition (...) will strengthen the Braime Group by securing this important source of supply, and by adding the margin made on the manufacturing of these products to the margin already made on the distribution and sales of our 4B electronic products.”

So if you hold the rest of the business flat and just layer the acquisition on top, the profit picture changes something like this:

One side note: the real 2026 numbers will look a bit different, because the deal only closed on 31 March 2026, so it will only be in the accounts for nine months of the year. I’ve also kept the core business completely flat, which is conservative given that revenue has grown for five straight years. And the £250k of acquisition costs is a one-off, so the underlying run-rate is actually a bit higher than what’s shown here. The calculation is just meant to give a rough sense of how the acquisition improves the earnings picture going forward.

What it does to the balance sheet

Before the acquisition, Braime’s balance sheet carried essentially no goodwill. That changes with the Don Electronics deal. With the fair value of consideration at about £11.5m against £9.0m of fair value net assets acquired, the deal adds ~£2.5m of goodwill.

On the asset side, you also get the £9.0m of fair value net assets added in.

On the liabilities side the change is more noticeable. You’ve got the new £5.2m HSBC loan, plus £4.9m of deferred consideration and around £1.6m of contingent consideration, so close to £11.7m of new obligations sitting alongside the existing debt.

You could say the extra ~£500k+ in profit each year comes to a certain extent from a more leveraged balance sheet.

Though that doesn’t account for the other, more structural benefits the acquisition brings.

The last thing worth saying is that the integration risk here is very low. These businesses have worked together for over 40 years, so there are no surprises about how they’re run and no friction about how decisions get made.

„The board is cognizant of integration risks and challenges that an acquisition brings. These are partly mitigated by the long-standing relationship between the parties and the contingent element of the consideration for the acquisition.“

Valuation

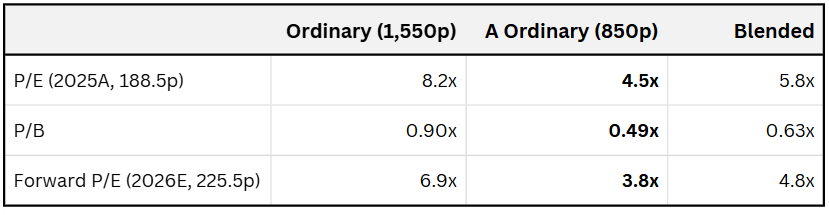

Over the past ten years, Braime has traded at an average of 14.7x earnings and 1.4x book value.

Neither is anywhere close to where it sits today.

At a blended market cap of £15.6m, the business trades at 5.8x earnings and 0.63x book value. But because of Braime’s dual share structure, that blended number isn’t really what you’d pay.

There are two classes of shares in issue:

480,000 Ordinary Shares

960,000 A Ordinary Shares

The only difference is that the A shares carry no voting rights. The claim on earnings, equity and dividends is exactly the same.

Economically, they’re identical.

But they trade at very different prices.

I’m focusing on the A shares here, because that’s where the discount is biggest.

So what you’ve got is a stable, profitable, consistently growing business with no dilution, decades of dividends, and an acquisition that should lift earnings further.

And yet it trades at multiples that look like the market is pricing in some kind of disaster.

The obvious question is: Why?

Why it’s cheap

As far as I can tell, there’s nothing actually wrong with this business. Operationally it’s fine.

The reasons for the low price are elsewhere.

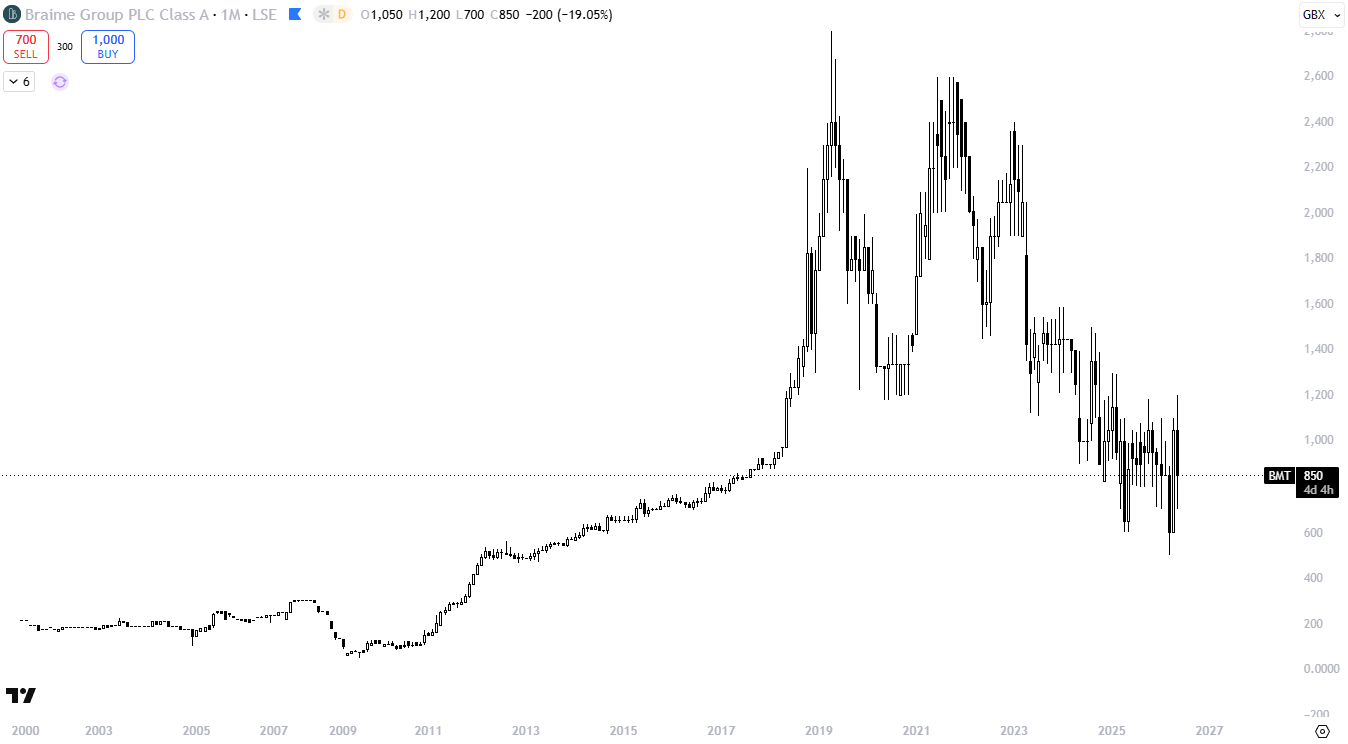

Take a look at the chart:

You’ll see that even though the stock had been volatile before, the real decline started right at the beginning of 2023.

‘Coincidentally,’ that’s exactly when the company announced its CEO transition.

On the 30th of January 2023, Braime announced that its long-serving CEO, Nicholas Braime, would step down. He’d held the role since 1987, a run of 36 years.

He knows the company inside and out, led it through decades of growth, and built close relationships with key suppliers along the way.

It’s completely normal for news like that to make investors nervous. If you don’t know much about the company or who’s taking over, the idea of losing that kind of experience and those relationships would worry anyone.

But the situation might be different than it first appears.

We know this business has been passed down through the family for generations, and it’s still in the founding family’s hands 138 years later. It’s basically a family heirloom that has fed the family for over a century.

I think it’s safe to assume they care about it deeply, and I think their actions back that up.

And looking more closely, the CEO transition doesn’t look like Nicholas simply walking away into retirement and being done with the business.

He remains Executive Chairman of the board, while his two sons Carl and Alan Braime, both of whom had been involved in the business for years, took over as joint CEOs. Both hold a substantial stake in the company.

So this isn’t Nicholas stepping aside.

He’s 76 years old. The thought process was probably something like: “I don’t have endless years left, so I’d rather hand the business over now, while I can still guide it as chairman, than keep going until I can’t and then figure it out from there.”

Carl and Alan also seem well suited for the role.

Carl has been with the group since the early 2000s as Group Sales Director, and Alan qualified as a chartered accountant at KPMG, spent four years there, and then joined the board in 2010 as commercial director.

„Both [Carl and Alan] have been on the Board since 2010 and have both experience and complementary skills... Together they are uniquely suited and well placed to transition the Group to its next phase of growth.“

So we can say this looks more like a planned, thoughtful succession, rather than a rushed handover into unfamiliar hands.

A further reason for the discount (this is more speculative) may be the broader macroeconomic environment, especially in Europe.

Since 2023, management has repeatedly voiced concerns about rising energy prices, the war in Ukraine and global tensions. They feared these factors could slow investment activity among customers and hurt margins.

I don’t want to get political or share macro opinions here (there are people far more qualified for that than me). But I think it’s worth pointing out that even though they’ve been nervous about their own numbers every year since early 2023, they’ve gone and posted back-to-back record revenue anyway.

That’s quite something in times of uncertainty.

And this ties back to Braime’s global diversification.

They are giving this same cautious outlook for next year as well.

„Today the current global economic background is significantly worse than 12 months ago and we are likely to face both inflation in costs and a reduction in investment led global demand due to increased business uncertainty.“

This misreading of the situation, or overreaction to it, pushed the share price down to levels last seen in 2017.

It’s a bit strange to look at what has actually happened to the business since then.

Since 2017:

Revenue is up 62%

Operating profit is up 90%

Net profit is up 70%

Book value has more than doubled, up 127%.

Revenue is more diversified. They’ve added subsidiaries in China, the UAE, Indonesia and Canada. And with the Don Electronics deal, the company now owns far more of its own value chain.

Which highlights the absurdity of the valuation.

A couple of other things

First, there is a point to be made about capital allocation.

I know management is very keen on their growth and expansion strategy, and rightly so. They’ve executed it well for decades and the recent acquisition came at a reasonable price.

But at 4 to 6x earnings, there’s a fair argument that buybacks would be a better use of capital right now.

Though to be fair, part of what they paid on the acquisition was likely a control premium, which you’d have to factor into that comparison.

Second, regarding other risks.

Even though I think this is a stable, well-run, diversified business, it’s not risk-free. There’s some integration risk on the acquisition, even if it’s lower than usual given the 40-year relationship. There’s the CEO transition, which I’ve already covered. There’s foreign exchange risk from operating across so many currencies, though they hedge where it matters. And there’s the broader macro backdrop, which management keeps reminding everyone about.

Final Thoughts

If you’ve been reading this blog for a while, this company might look a little familiar. That’s because I actually wrote about them a year ago. I don’t normally do this. In fact, this is the first time I’ve ever written about a stock a second time, as I like to provide new value with every writeup.

But the situation here has changed so significantly through the recent acquisition that I simply had to. This wasn’t just some special dividend where the rest of the thesis stayed the same. There were real, meaningful changes. And after reading my old writeup, I thought I really could provide additional value.

I liked it back then. I like it more now.

It’s a classic case of cheap because the market is misunderstanding the situation.

And as Burry said:

Where there’s misunderstanding, there is value.

Disclaimer: The information provided in this newsletter is intended for informational and educational purposes only. It does not constitute financial, investment, legal, or tax advice. All analyses, opinions, and interpretations reflect my personal views at the time of publication and are provided without reference to the individual circumstances or objectives of any reader. All analyses, information, and opinions have been prepared with great care. Nevertheless, no guarantee can be given as to the accuracy, completeness, or timeliness of the information provided. Use of the content is at the user’s own risk. Investing in securities involves risk, including the possible loss of capital. Readers should conduct their own research and, if necessary, consult a qualified professional before making investment decisions.

Noel - Nice find and comprehensive pitch. TY