A Family Business at a Bargain Price

4.1x earnings. 0.41x book value.

Key Metrics:

4.1x earnings

0.41x book value

3.31x EV/EBITDA

30+ years dividend record

In his early days, Buffett spent endless hours flipping through the Moody’s Manuals. Thousands of pages of financial data on every listed company. He read them back and forth. Line by line.

Sometimes, hidden among thousands of stocks, he would find a tiny, illiquid business trading at an absurd discount. Too small for Wall Street. Too boring for big funds.

But cheap. Very cheap.

From 1952 to 1962 Buffet compounded his money at 48% per year by finding these mispriced gems.

With today’s technology, screeners, and algorithms you’d think opportunities like that no longer exist.

Well, they do.

You just have to dig deeper.

I found today‘s stock after going through hundreds if not thousands of little microcaps. Most were uninvestable. But this one stood out.

It’s a tiny, illiquid, and overlooked family business founded in 1888, trading at a deep discount.

Let’s take a closer look.

Braime Group PLC (BMT)

Braime Group PLC (BMT) is a British manufacturer with over 130 years of experience. The company operates globally, with its core business split into two parts.

First, the 4B Division

This segment produces and sells everything needed to move and monitor bulk materials safely and efficiently—worldwide. That includes elevator buckets, belts, chains, sensors, and other components. Customers range from farmers and silo operators to ports, basically anyone who moves heavy stuff.

Second, Braime Pressings

Here, the company produces precision steel parts, mainly for the automotive and construction industries.

Their core strategy makes Braime stand out. It consists of high reinvestment into the business. They spend heavily on new machinery, technology, land, and capacity expansion.

Just take a look at their capital expenditures:

2022: £2.8M

2023: £1.6M

2024: £1.4M

That’s a lot, considering their market cap is just £13.6M.

One of the more interesting investments in 2024 was the purchase of four acres of land next to their U.S. warehouse in Illinois.

„Our strategy remains largely unchanged, continuing to invest in constantly improving our production processes and exploring new global markets for our niche products and developing new innovations for our customers’ engineering challenges.“

To say the least: It works. And it works well. In the following section you will see why.

Beyond the numbers, this strategy also shows their long-term thinking, and care about the future of the business.

Let‘s walk through the numbers:

(Note: All figures are in British Pounds.)

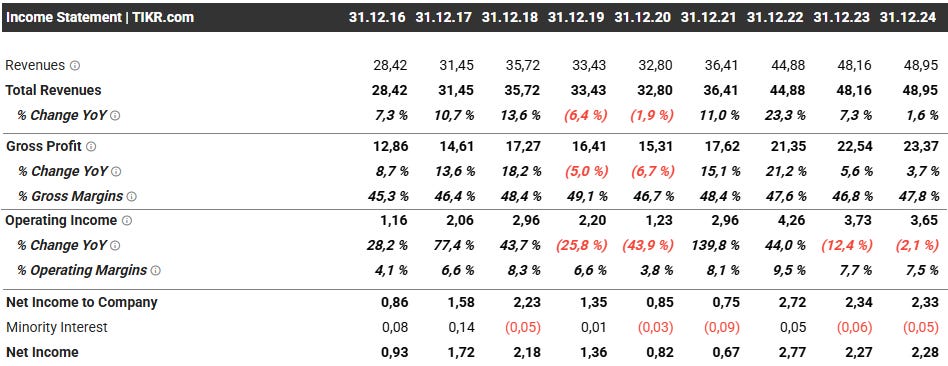

Income Statement

→ Income statement excerpts

Aside from a small dip during 2019–2020, revenue has been growing consistently for the past decade, with YoY growth since COVID. However, recently growth slowed down a bit. Mostly due to broader market conditions in Europe and the impact of the war in Ukraine. I’ll go into more detail on that in a second.

Gross profit moved in line with revenue.

Operating income, however, looked a little different. Margins have been under pressure. Rising costs, especially energy and logistics, squeezed profitability over the last few years, leading to slightly lower operating and net income.

Still, here’s something I really like:

Braime has paid a dividend every year for over 30 years, except during the global financial crisis. It’s not a huge dividend. At £0.15 per share, the yield is around 2.2–2.5%. But that kind of consistency says a lot. Especially for a company this small.

Regarding the revenue, I want to give a little more detail on how it’s broken down:

The 4B Division is clearly the backbone of the business.

In 2024, it generated £43.7M in sales, about 89% of total revenue.

Braime Pressings, by comparison, brought in just £5.2M, about 11%.

„Our 4B division maintains its competitive edge in a price sensitive market“

The global allocation is also pretty interesting.

America (North & South):

Revenue in 2023 and 2024 came in at £23M. Solid and stable.

Yet from 2022 to 2023, this region grew +22%.

Europe:

Revenue here has been flat. The company cites weak investment due to war, energy prices, and inflation.

„Sales in the UK and Europe were also in line with prior year as investment has remained subdued against the backdrop of the ongoing war in Ukraine, rising energy costs and continued inflation.“

Africa:

Up +17% in 2024.

Australasia:

Up +14% in 2024.

This tells us two important things:

First, Braime is geographically diversified, that’s a strength in itself.

Second, their expansion strategy is working.

Because they invested in growth markets, they’ve been able to post record sales for the past 3 years, even while Europe stagnates.

Balance Sheet

→ Balance sheet excerpts

Braime’s balance sheet looks solid. They hold a healthy amount of cash, carry very little debt, and have zero goodwill.

Their debt-to-net-current-asset ratio sits at just 22%. That’s something any Graham die-hard would find comfort in.

Now, I know Graham himself tolerated ratios as high as 100%. But I still prefer low to no debt.

Debt is leverage. And leverage magnifies outcomes. Good outcomes become great, and bad outcomes can turn into disasters. Given that this company is already cheap, any re-rating towards a more reasonable valuation would deliver strong returns. So why introduce any more leverage? I like my returns without additional risk.

Another point worth highlighting: Equity has been growing steadily, compounding at an average rate of ~23% per year over the past decade. A nice value creation happening in the background.

So after reviewing the income statement, the company’s reinvestment strategy, and now the balance sheet, it should be clear that we’re looking at a stable, growing, and well-managed business.

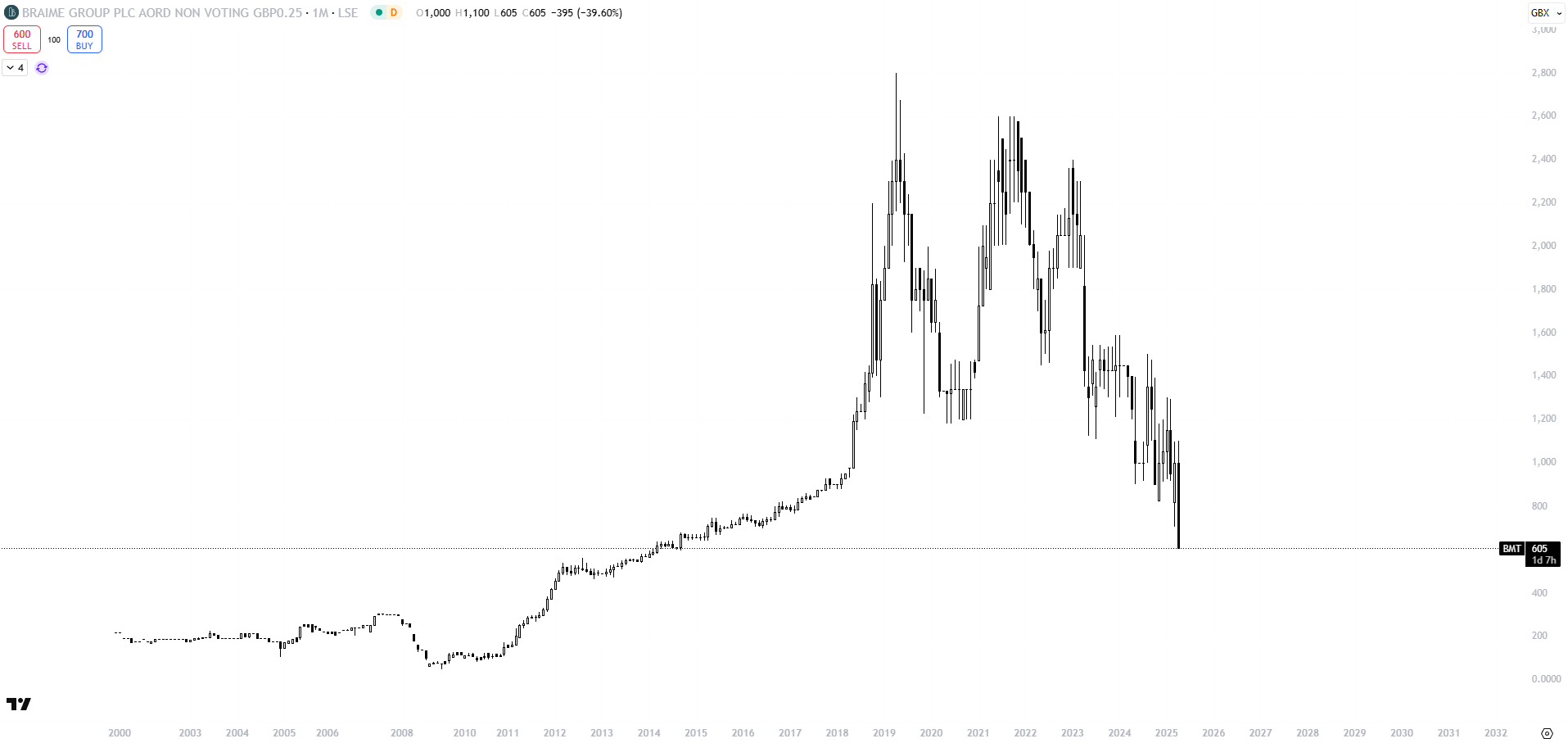

And yet, the chart looks like this:

Valuation

The stock is currently trading at prices last seen in 2014–2016. The market is effectively valuing the company the same as it did back then. Yet looking at the numbers, this pricing makes no sense.

Since 2016:

Revenue has nearly doubled.

Operating income has more than tripled.

Book value is also more than 2x higher.

And yet the market is valuing the company today as if nothing has changed.

Here are the average valuation multiples over the past 10 years:

Average Price-to-Book (P/B): 1.4x

Average Price-to-Earnings (P/E): 13.56x

Even though the industry average trades even higher (around 17.5x earnings), we’re still looking at a small microcap, so a small haircut is justified.

But still, here’s where we are today:

0.41x book value

4.11x earnings

Even with all the usual small-cap caveats, that’s a steep discount.

And with a market cap of just £13.68M, we’re almost sitting at net current asset value.

NCAV = Current Assets – Total Liabilities

= £24.79M – £13.03M = £11.76M

Even though were looking at a profitable, dividend-paying, growing business, the market is pricing the entire company just slightly above its liquidation value.

Now, I don’t really like tossing out price targets. But even a partial reversion to historical multiples would imply meaningful upside.

Let’s take a closer look at why investors are nervous, and what’s pushing the stock into discount territory.

Reason for Discount

Based on my research and looking at the time when investors started to sell, I see two key reasons behind the market’s behaviour:

The first is the CEO transition.

On January 30th, 2023, Braime Group announced that its long-serving CEO, Nicholas Braime, would step down.

He had been in the role since 1987. A full 38 years.

That kind of headline naturally makes investors nervous. Nicholas knows the company inside and out and has led it through decades of successful growth, especially in recent years. Over those decades, he built close relationships with key suppliers. Losing that kind of experience and network would concern anyone.

But the situation might not be as bad as it seems at first glance.

Nicholas didn’t just walk away. He remains on the board as Executive Chairman. While his two sons, Carl and Alan Braime, who have both been involved in the business for years, now act as joint CEOs.

Since Braime is very much a family business, and all three hold substantial ownership in the company, it’s clear that Nicholas isn’t just stepping away to enjoy retirement. It looks like he wants to stay involved, provide guidance, and use his decades of knowledge and relationships to make sure the business continues to thrive under new leadership.

Looking at the background of Carl and Alan Braime, they seem well suited for the role.

„Both [Carl and Alan] have been on the Board since 2010 and have both experience and complimentary skills, including an in-depth understanding of the industries in which the business is involved and the needs of our key stakeholders. Together they are uniquely suited and well placed to transition the Group to its next phase of growth.“

~ Nicholas Braime

Carl Braime has been with the Group since 2003, serving as Group Sales Director. Alan Braime worked as a chartered accountant at KPMG for four years before joining the board in 2010 as commercial director.

In short: this is a thoughtful succession, not a rushed handover.

To me, it shows that management genuinely cares about continuity and long-term success.

The second reason for the discount is the current macroeconomic environment, especially in Europe. Starting in early 2023, management began voicing concerns more openly in their investor communications.

They highlighted risks around rising energy prices, the war in Ukraine, and global tensions, especially between the U.S. and China. They feared that these factors could slow investment activity among customers and hurt margins.

In early 2023, they wrote:

“Repeating 2022’s record numbers might be overly ambitious.”

And yet, they pulled it off.

Sales grew 7.3% YoY.

For 2024, they were again conservative:

“Much of the world economy is currently either in recession, or at risk of being in recession… this will inevitably affect our own performance in 2024.”

And it did.

YoY growth slowed to 1.6%.

Yet it’s still another record year.

This can be directly attributed to Braime’s global diversification. Because of which Braime’s business kept growing, even as Europe stalled.

„While demand was badly affected in some areas by the invasion of Ukraine by Russia, the investment in new plant and machinery was very largely transferred elsewhere and the global nature of our business profile remains one of the key underlying strengths of our multinational trading business“

To me, that kind of honest, cautious outlook is not a weakness, it’s a sign of responsible leadership. It shows a management team that cares about the company’s future, not just short-term share price performance.

So to sum it up, the two main reasons for the current discount are:

The transition to a new joint-CEO structure.

Broader macro uncertainty, especially in Europe.

In my eyes, these are also the main risks facing the company right now.

Yes, there are some more general risks too, like exchange rate risk (which is properly hedged), and customer concentration (with one client accounting for 10.5% of revenue). But overall I would consider the business well diversified, especially by region and segment.

„The two segments of the Group are very different operations and serve different markets, however together they provide diversification, strength and balance to the Group and their activities.“

But still, management remains cautious:

„However, the current economic and geo-political situation is more fraught than at any time in my lifetime. So the “Outlook” currently for the business is simply and frankly one of uncertainty.“ ~ Nicholas Braime, Chairman, former CEO

But with year-over-year growth, resilient margins, consistent dividends, and successful global expansion, the business is clearly built to last.

Delivering record numbers in uncertain times is a very good sign. To me, this speaks of a durable, recession-resistant company. And when market conditions shift in its favour, the company is positioned to thrive.

„This is again a record as the business has continued to see year on year growth in sales over the last 5 years, navigating our way through some turbulent global economic conditions since the pandemic.“

Final Thoughts

With Braime, we’re looking at a solid, profitable company.

One with strong fundamentals, a clean balance sheet, growing sales and equity, and a long history of stable operations.

A business that’s been pushed into discount territory, not because of a failing product, broken margins, or shady management, but because investors got nervous.

Yes, the concerns are valid.

But the numbers tell a different story.

When you strip away the noise, you see a well-run, globally diversified manufacturer, trading well below its fair value.

To me, this is what value investing is all about:

Buying a solid business for less than it’s worth, simply because the market isn’t paying attention.

And with a clear margin of safety, that’s a bet I’m happy to take.

Side note: In this write-up, I tried something new: I kept it as reader-friendly and time-efficient as possible, focusing only on what matters for the thesis, without loading it up with secondary details. There are more topics I looked into, like management compensation, hedging, and other smaller points. Even though I didn’t cover them in detail here, I’ve checked them thoroughly and see no red flags.

If you're curious about specific aspects, feel free to ask in the comments. I’m happy to share more details.

Please let me know what you think of this approach!

Disclaimer: This content is for informational and educational purposes only and should not be considered investment advice. I’m just sharing my thoughts—not telling you what to do with your money. Some of what I write may turn out to be wrong. Always do your own research.

Excellent post Noel, does a great job of piquing interest and conveying the key details. One thing that comes to mind is the competitive situation - do they have any pricing power? Is there any threat of manufacturing from low-cost countries competing?

I replied to the note you originally put out on this saying I was sure there'd be a catch. I'll have a proper look in a couple weeks, but right now I can't see anything obvious - looks like a screamer. Good find.

What's the situation with the BMT/BMTO double listing?