A Cheap and Growing Microcap You've Never Heard Of

Debt-free. Aligned management. 4x earnings.

Key Metrics:

4x earnings

Aligned Management

Debt-free

Have you ever heard of the OTC-X exchange?

Well, I hadn’t.

At least not until recently.

It’s a tiny Swiss OTC exchange for unlisted securities, run by a regional bank called BEKB.

When I first came across it, I started clicking through some of the stocks listed there.

And I quickly noticed something.

I had no idea who any of these companies were. Not one name rang a bell.

None of them showed up in any screener I’d ever used.

That, of course, sparked my interest.

So I went through all of them.

As with most exchanges, the majority of what’s listed is stuff you wouldn’t want to touch. Money-losing operations, shrinking businesses, absurd valuations.

But a couple were interesting.

One in particular.

The stock I am writing about today.

Luftseilbahn Grindelwald-Pfingstegg AG.

A small tourism company in the Swiss Alps. It runs a cable car, an alpine coaster, and a fly-line on a mountain above the village of Grindelwald.

Visitors take the cable car up. They ride the coaster down. They fly through the forest on the fly-line. They pay for each ride.

What makes it interesting is not the business model, but what happened over the past six years.

Revenue nearly tripled. Margins expanded dramatically. The bank loan got paid off in full. A new CEO took over. They reinstated a dividend. And the stock still trades at 4x earnings.

That kind of setup is something you only find at an exchange nobody else is looking at.

There’s a catch, though.

The opportunity that comes with obscurity has a price.

This stock is really illiquid.

Shares almost never trade.

Only two shares have changed hands so far this year. Six in all of 2025.

It’s also genuinely difficult to buy. Easier if you’re in Europe, but I honestly don’t know how you’d get it done from the US.

With that out of the way, let’s take a closer look.

Luftseilbahn Grindelwald-Pfingstegg AG

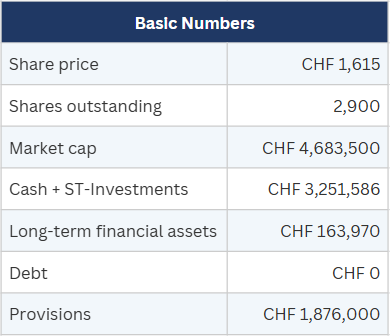

ISIN: CH0002052782 | Market Cap: ~CHF 4.7M | Website

Pfingsteggbahn was founded in 1967 and sits at the base of the Mettenberg in Grindelwald, one of Switzerland’s most visited mountain villages. The broader Jungfrau Region draws millions of tourists every year.

The company runs three attractions.

The cable car is the core product. It’s a pendulum-style aerial tramway that carries visitors from Grindelwald at 1,027 meters up to the Pfingstegg station at 1,387 meters. The ride covers 360 meters of elevation in about three minutes. Capacity is 450 people per hour. It accounts for 65% of revenue.

The alpine coaster opened in 1999. It’s a 725-meter stainless steel slide that winds down the mountain at speeds up to 37 km/h. The company markets this as its unique selling point. It generates about 21% of revenue.

The fly-line opened in October 2019. It’s a rail-guided ride through the forest with an automatic return system that brings riders back to the start. The company says it’s the only fly-line in the world with this feature. It now contributes about 14% of revenue.

The remaining 2% or so comes from freight transport, special cable car dinners, events, and other small items.

This is a pure summer business.

The attractions run from May to October, with somewhere between 156 and 170 operating days a year. The rest of the year is maintenance and preparation.

That also means revenue is almost entirely dependent on summer weather. The years 2018, 2019, 2022, 2023, and 2024, all benefited from above-average conditions.

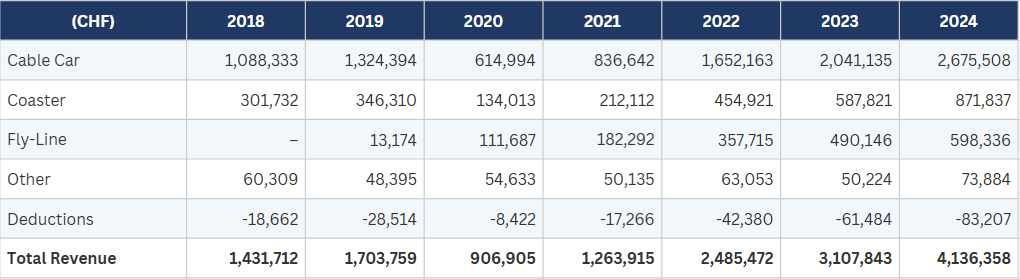

The Revenue Story

Here’s where it gets interesting.

(All figures in CHF)

Revenue grew from CHF 1.43 million in 2018 to CHF 4.14 million in 2024. That’s nearly a tripling, at a compound annual growth rate of ~19%.

If you start from 2020, the numbers look even more impressive. Revenue went from CHF 907k to CHF 4.1 million. A 4.6x increase.

But context matters.

COVID hit this business hard. Switzerland banned leisure facilities in spring 2020. The cable car ran only 128 days instead of 170. International tourists largely disappeared, and revenue dropped 47% in a single year.

2021 wasn’t much better. Restrictions were still in place, the season was still shortened, and international visitors were still mostly gone. Revenue recovered somewhat but remained 26% below the 2019 record.

Then things broke loose.

2022 was the first fully normal post-COVID season. Revenue nearly doubled year-over-year to CHF 2.5 million, blowing past the 2019 record of CHF 1.7 million by 46%.

But this wasn’t just a bounce-back.

Three things happened at once.

First, the fly-line had its first full seasons. It had barely opened in 2019, running just 16 days in October, and was hobbled by COVID in 2020 and 2021. By 2022 it was running at full capacity, contributing CHF 358k.

Second, a new CEO took over in early 2023. Remo Spieler replaced the long-time manager Roger Bischoff. Spieler came from a tourism and marketing background. Under his leadership, the company raised prices, intensified marketing, and pushed for higher visitor volumes.

Third, the broader shift toward outdoor recreation and domestic tourism in Switzerland, paired with excellent summer weather, lifted the entire Jungfrau Region.

The combination of higher prices and more visitors created disproportionate revenue growth. Revenue climbed to CHF 3.1 million in 2023 and CHF 4.1 million in 2024. Each year a new all-time record.

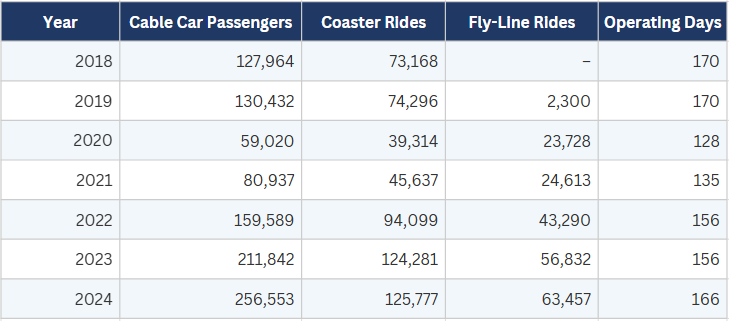

The visitor numbers tell the same story:

Cable car passengers have doubled since the pre-COVID peak. Coaster rides are up 69%. The fly-line has grown from nothing to over 63,000 rides per year.

Worth noting too is how the fly-line changed the revenue mix.

In 2018, the cable car accounted for 76% of total revenue. By 2024 that share had fallen to 65%, with the coaster and fly-line together making up 36%. That diversification makes the business more resilient to any single disruption.

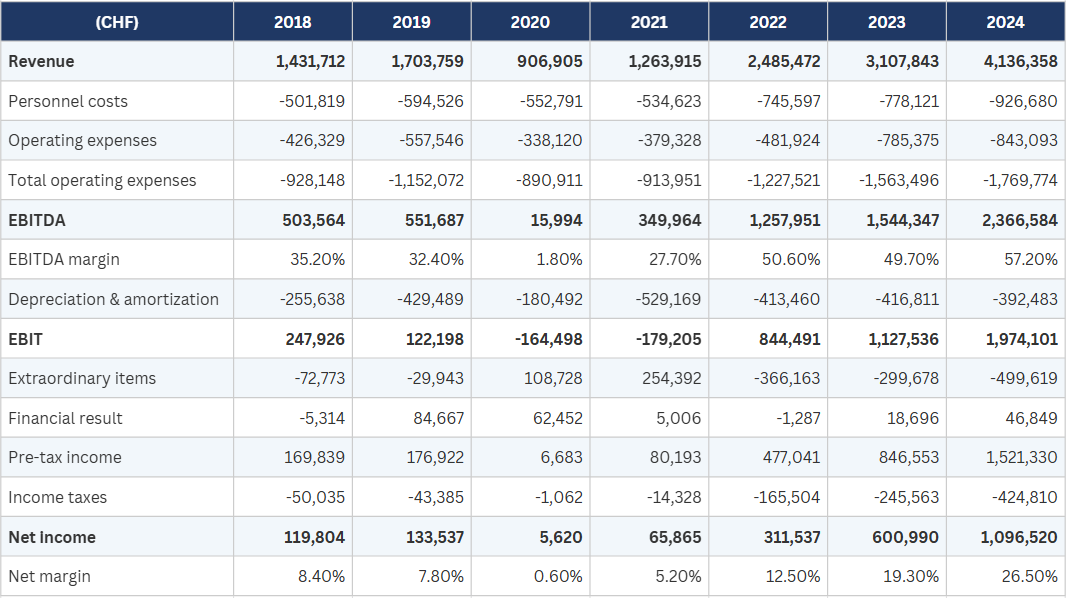

Margins

The margin expansion might be the most interesting part of this story.

EBITDA margins went from 35% in 2018 to 57% in 2024. Net margins more than tripled, from 8.4% to 26.5%.

The driver is operating leverage.

The cost structure here is mostly fixed. The cable car runs whether there are 50 passengers or 500. The coaster needs a staff member regardless of how many riders show up. Insurance, maintenance, and rent don’t move much with volume.

So when revenue doubles, costs don’t.

Staff costs as a share of revenue fell from 35% in 2018 to 22% in 2024. And that happened even as the company hired more people and total payroll grew from CHF 502k to CHF 927k in absolute terms.

The result is that earnings grow faster than revenue. From 2019 to 2024, revenue grew 143%. Net income grew 720%.

One more thing worth understanding. The reported net income is actually understated, and intentionally so.

Every year, the company books a charge of CHF 300,000 to 500,000 for what they call renewal provisions. These are voluntary allocations to a reserve fund for future capital investments in the cable car infrastructure.

They show up as an expense, but they are not a cash cost. The money stays in the business. It’s essentially management saying, “Let’s set aside cash for the next big renovation now, so we don’t have to borrow when the time comes.”

In 2024, the charge was CHF 500,000. Without it, pre-tax income would have been CHF 2.0 million instead of CHF 1.5 million.

I’ll come back to this in the next section.

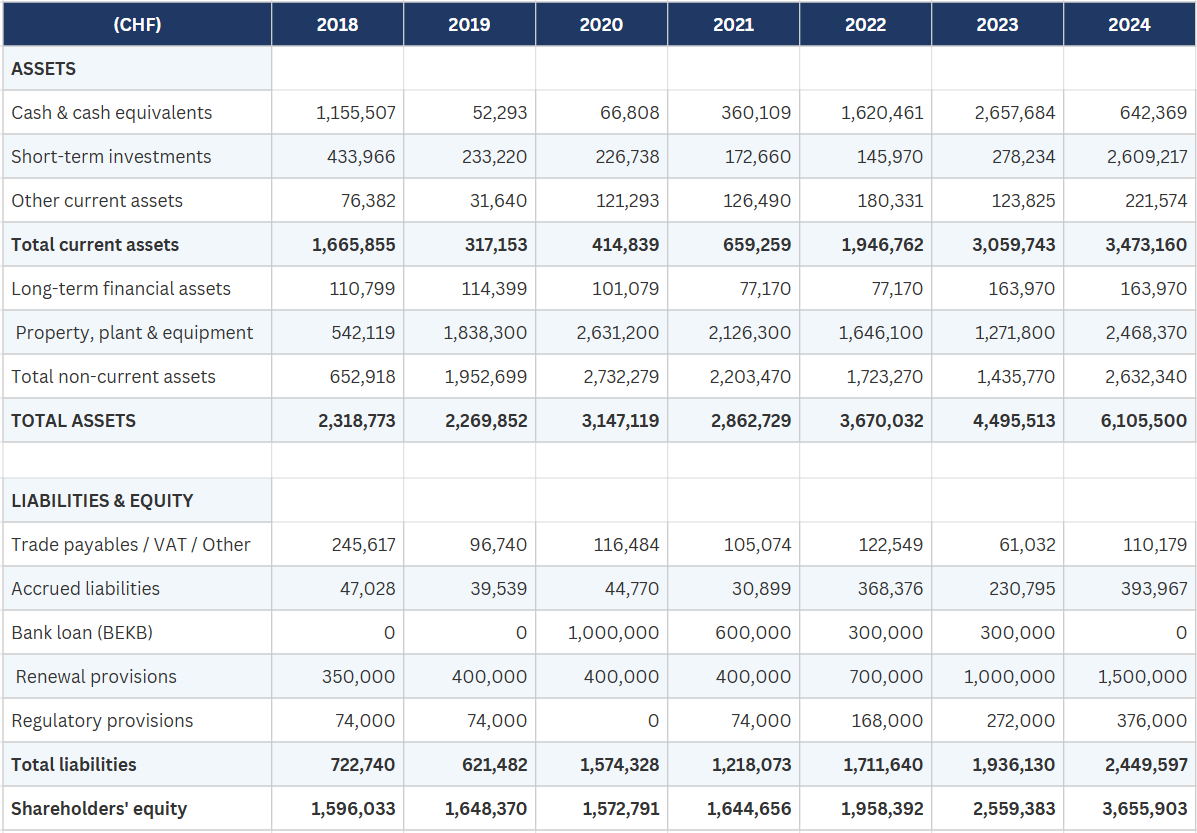

Balance Sheet

The balance sheet has changed dramatically since 2020.

Here’s the simplified version:

Start with the debt, because there isn’t any.

In 2020, with COVID raging, Pfingsteggbahn took out a CHF 1 million bank loan from BEKB. That was the only long-term debt the company has ever carried in recent history. They paid it back steadily over four years and retired the last of it in 2024. The company is now completely debt-free.

Then there’s the cash. Cash and short-term investments together come to CHF 3.25 million. The entire market cap is CHF 4.68 million. So you’re paying CHF 4.68 million for a business where CHF 3.25 million of that is just sitting in liquid assets.

Now, the provisions. This is the part that takes a little explaining. The largest liability on the balance sheet is CHF 1.5 million in renewal provisions and CHF 376k in regulatory provisions.

These are not obligations to outside creditors. They are internally created reserves. The renewal provision is money management voluntarily set aside to fund future capital expenditures.

The regulatory provision is required under Swiss transport law, which mandates that operators maintain the physical integrity of their infrastructure over time.

The question is: are these liabilities or a form of hidden equity?

I’d argue the latter. They don’t represent money owed to anyone. They represent retained earnings that management has earmarked for future use.

If this company shut down tomorrow, that money would go to shareholders.

That said, I treat them both ways in the valuation section. Once as debt-like, and once as quasi-equity.

Valuation

Let’s put some numbers to it.

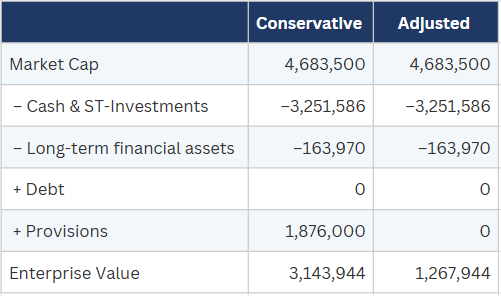

Enterprise value depends on how you treat the provisions.

Treat them as liabilities and the EV is CHF 3.14 million. Treat them as quasi-equity, and the EV drops to CHF 1.27 million.

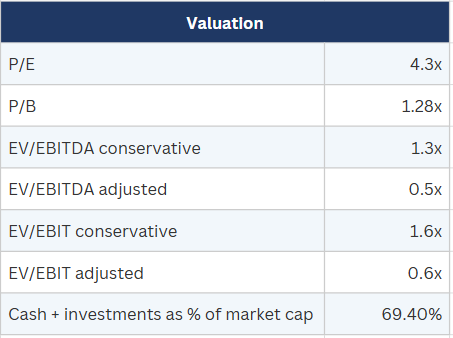

The multiples look like this.

So the stock trades at a 4.3x P/E, and an EV/EBIT between 0.6x and 1.6x, with 69% of the market cap covered by cash and investments.

The company is also paying its first dividend since 2019. The board proposed CHF 70 per share plus a CHF 35 bonus dividend for a total of CHF 105. That’s a 6.5% yield at today’s price.

The dividend was suspended during COVID. After that, the cash went toward paying down debt and building reserves. Only now, with the balance sheet clean and the provisions funded, did management restart the payout. That’s exactly the right order of priorities.

So why is this so cheap?

Three reasons.

First, it trades on OTC-X. The exchange is tiny and almost completely unknown. With only 2,900 shares outstanding and essentially no daily volume, most investors will never come across it.

Second, there is no coverage. Nobody writes about this stock. It doesn’t show up in any screener, and the annual report is published in German only.

Third, the share price itself is a barrier. At CHF 1,615 per share, you need CHF 16,150 just to buy ten shares. That puts off smaller investors. And anyone who does buy in knows the position will be illiquid no matter what.

Put it all together and you have a stock that almost no one can find, almost no one can easily buy, and almost no one has written about. That’s why it’s cheap.

Management

Good businesses run by bad managers are rarely good investments.

For this reason, I want to highlight what the management team has done, especially since the CEO change in early 2023.

They paid off all debt. The company went from leveraged to debt-free in four years.

They raised prices. Combined with higher visitor volumes, that created a double tailwind for revenue.

They invested in the core business with a CHF 1.59 million cable car renovation in 2024/25, funded entirely from cash flow. They also installed a photovoltaic system on the valley station roof.

They kept building reserves.

They restarted the dividend. (Only after the balance sheet was clean. Not before.)

And they grew marketing spend from CHF 34k in 2021 to CHF 78k in 2024.

To me, that’s a picture of aligned management. People who understand shareholder value and are focused on growing the business the right way.

Risks

Beyond the obscurity of the listing, there are a few real risks worth mentioning.

The business is heavily weather-dependent. This is a summer-only, outdoor business. A bad summer can materially impact earnings. In 2021, there were only 56 days of good weather versus 88 in 2023.

The second is concentration. There is only a single location. Everything happens on one mountain. A natural disaster, like a landslide, avalanche, or an infrastructure failure, could shut the operation for an extended period.

And then there’s the illiquidity, which I’ve already mentioned but is worth repeating here as a genuine risk. With 2,900 shares and almost no trading volume, you cannot exit this position quickly. If something goes wrong, operationally or otherwise, you are largely stuck.

Final Thoughts

This is a straightforward business.

A cable car, a coaster, and a fly-line on a mountain in the Swiss Alps.

Revenue has nearly tripled since the pre-COVID peak. The fly-line added a third pillar to the business. A new CEO came in and raised prices, grew volumes, and doubled marketing spend. EBITDA margins expanded from 35% to 57%.

The balance sheet is clean, with no debt, and CHF 3.3 million in cash and investments against a CHF 4.7 million market cap. Provisions that look like liabilities but function more like retained earnings.

And the stock trades at 4x earnings.

The cash and investments alone cover nearly 70% of the market cap, and the company is paying a 6.5% dividend for the first time in five years.

The main risk is that this is a tiny, illiquid stock on an obscure Swiss exchange. You can’t build a large position easily. And if something goes wrong, like a bad summer, or a natural disaster, there’s no way to exit quickly.

But at this price, you don’t need things to go perfectly. Even if earnings fell back to 2022 levels, the stock would still be cheap relative to what’s sitting on the balance sheet.

This combination of revenue growth, margin expansion, debt payoff, capital returns, aligned management, and a cheap valuation is exactly the kind of thing you can find when you look where others don’t.

Side Note:

Two other names from OTC-X caught my attention while going through the exchange. Neither is as compelling as Pfingsteggbahn, but both are worth a mention.

The first is SWS Medien. A tiny printing business with a market cap of CHF 2.1 million.

Revenue is declining and the business is barely profitable. What makes it interesting is the net cash position of CHF 5.5 million against a CHF 2.1 million market cap.

The second is Rigi Bahnen AG. This one is a little bigger and has a market cap of CHF 48 million.

It operates mountain railways on Mount Rigi and has been around for about 150 years.

Revenue and earnings have grown strongly over the past couple of years. There’s some debt on the balance sheet, but it trades at 7x earnings and slightly below book value.

Disclaimer: The information provided in this newsletter is intended for informational and educational purposes only. It does not constitute financial, investment, legal, or tax advice. All analyses, opinions, and interpretations reflect my personal views at the time of publication and are provided without reference to the individual circumstances or objectives of any reader. All analyses, information, and opinions have been prepared with great care. Nevertheless, no guarantee can be given as to the accuracy, completeness, or timeliness of the information provided. Use of the content is at the user’s own risk. Investing in securities involves risk, including the possible loss of capital. Readers should conduct their own research and, if necessary, consult a qualified professional before making investment decisions.

Good stuff! Where I can put my hands on these names , not available on IBKR nor Degiro ?