A Net-Net With Insider Buying

0.53x NCAV. 1.42x EV/EBIT.

Key Metrics:

0.53x NCAV

1.42x EV/EBIT

0.42x Book

No Bank Debt

In the 1950s, Warren Buffett was compounding at 50 to 60% a year.

He has called it the best decade of his investing life.

And he was not doing it by finding great businesses at fair prices. He was doing it by buying cigar butts.

Stocks so cheap, they trade below what you would get back if you simply liquidated the whole thing.

The name comes from the image itself.

Picture someone walking down the street, smoking a cigar, and tossing it before it’s finished. Most people step over it. But someone picks it up, because it still has one puff left. And because they found it on the ground, that last puff costs them nothing. It is pure profit.

The business might not be growing. It might not be pretty. But the price is so low that even in a wind-down, you come out ahead.

Today’s stock is exactly that.

A cigar butt, in the most classic sense.

A profitable business trading at a meaningful discount to its own liquidation value.

And there is one more thing.

The insiders are buying.

The family that controls this company has been purchasing shares on the open market at prices close to where the stock trades today.

Insider selling can happen for all kinds of reasons, but insider buying basically means one thing: they think the stock is cheap.

At 53% of net current asset value and 1.4x EV/EBIT, it is not hard to see why.

Passat SA

Ticker: ALPAS (formerly PSAT) Market cap: €17.3M

Passat is a French micro-cap. And it’s in a business you’ve probably subconsciously noticed somewhere before.

It’s called “image-assisted selling.”

This is not teleshopping in the TV-channel sense.

They place video screens directly inside French retail chains like Carrefour, Leclerc, and Castorama. The screens play short product demos. A shopper walks by, sees the product in action, and buys it right off the shelf.

Passat doesn’t own a single store, and they don’t run checkouts. They curate the product catalog, make the videos, set up the displays, and stock the retailer’s shelves.

The company was founded in 1987 and sources consumer products from around the world: kitchen gadgets, cleaning supplies, garden tools, hand tools, hair straighteners. Things that sell for €10 to €50.

In 2022, Passat acquired 65% of a French-Belgian group called Best of TV.

Best of TV operates in the same image-assisted selling niche but with complementary products. Today it generates about 40% of group revenue and most of the group’s operating profit.

Outside France, Passat has small operations in Spain, Portugal, and the US. The US business is effectively a single product, a branded chimney-sweeping log, sold through a commercial agent. It’s highly seasonal and has been slowly shrinking for years.

The Income Statement

This is the least attractive part of the story, and there are a couple of things worth understanding before we look at the numbers.

The operating reality inside Passat has shifted since the Best of TV acquisition in 2022. For the better, I should add.

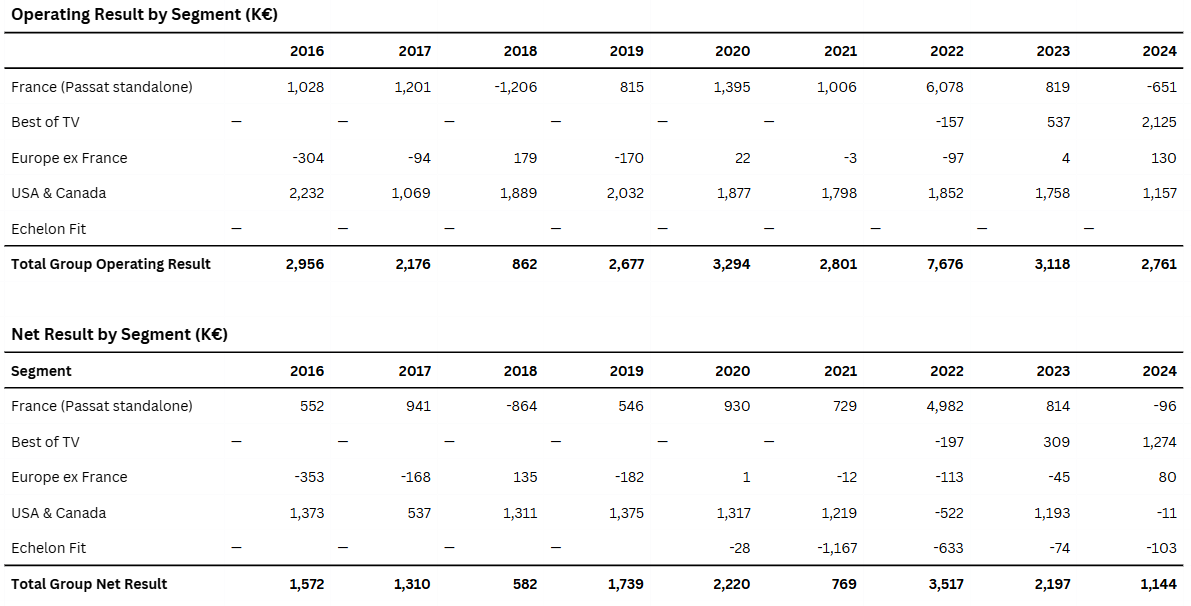

The segment breakdown makes that clear:

France, the business Passat has been running for 37 years, swung from 1 million operating profit in 2023 to a €0.6 million operating loss in 2024.

Without Best of TV, which was only acquired three years ago, the group picture would look considerably worse.

In 2024, Best of TV contributed €26.1 million of revenue and €2.1 million of operating profit. It is now the single largest profit contributor in the group.

The US business has basically halved its operating result since 2016.

It was net loss making at the bottom line in 2024 due to goodwill and financial impairments on the US holding structure.

And then there’s the Echelon Fit joint venture. Passat bought into a connected fitness business (bikes, treadmills, rowing machines) during COVID lockdowns, basically at the peak of the at-home fitness cycle. The timing was about as bad as it gets. Passat has already booked a €3.4 million provision against its carrying value.

Now to the full picture:

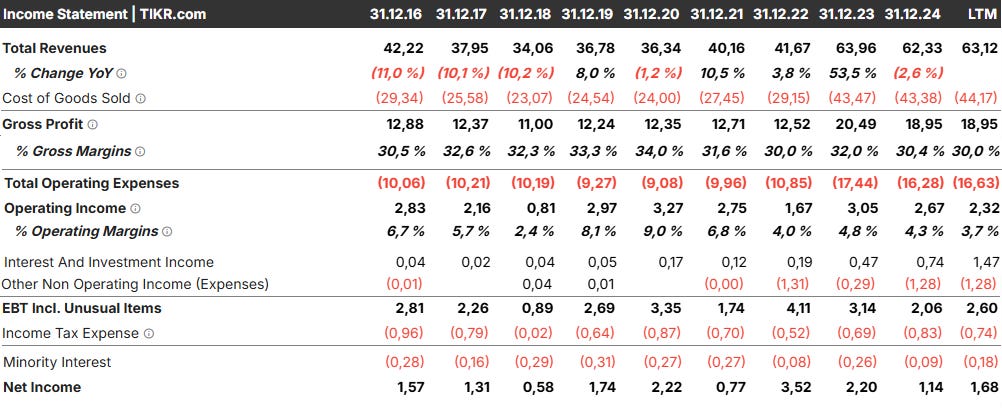

Consolidated revenue was €42 million in 2016, dipped to €34 million in 2018, climbed back to €42 million by 2022, and jumped to €64 million in 2023.

That jump was entirely due to consolidating Best of TV.

Management said so themselves, on a like-for-like basis, 2023 revenue was actually down 4% from 2022.

“Consolidated revenue of €63,956,000, up 53.5% from 2022. On a like-for-like basis (excluding BEST OF TV), revenue decreased by 4%” – 2023 annual report

Since the acquisition is now in the base, revenue has been stagnant. The first half of 2025 grew 2.7% yoy, but that’s inside the noise band.

What deserves a bit more attention is what’s happening to margins.

Operating margin has compressed from 7-9%, to 4.4% in 2024, and just 1.9% in H1 2025.

The reason is that Best of TV runs with higher marketing spend and more freight than the legacy Passat business. On top of that, group personnel costs and external expenses are rising.

The underlying message is that the acquired BOTV business, now the group’s main profit contributor, runs at a structurally lower margin than legacy Passat France did when it was functioning well.

So one could say the group has in effect traded volume and diversification for margin density.

H1 2025 confirms the trend. France operating profit was €551,000, down from €995,000 a year earlier. Headline net income turned positive (€0.35m vs a €0.18m loss) but only because H1 2024 included a €921,000 one-off impairment on the US Echelon stake.

However, since the US chimney log business is seasonal and runs its commercial season from October through January, H1 doesn’t really factor in results from the US business. H2 should look better because of that, on a net income basis.

The company also mentions this themselves in their half year report:

“The marketing campaign only starts in October and ends in January, so sales of this period are not significant.”

But seasonality doesn’t explain what’s happening in France.

That said, despite the recent pressure, the group has been operationally and net income positive every year since at least 2009. That’s not nothing.

The Balance Sheet

This is where Passat gets interesting.

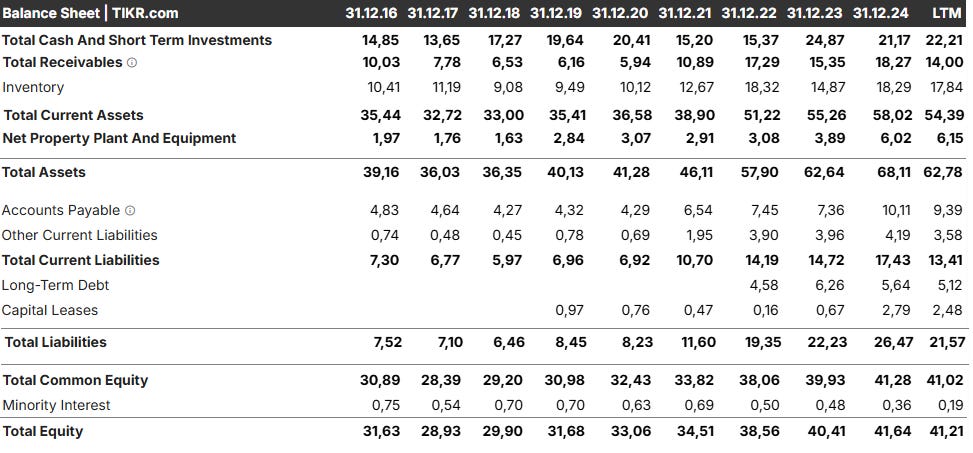

At the end of H1 2025, Passat was sitting on €22.2 million in cash and marketable securities. The whole company trades for €17.3 million.

And there’s no bank debt. Management repeats the same sentence in every annual report they publish:

“The Passat Group presents a healthy balance sheet, characterised by zero short-term and long-term bank indebtedness.”

That has been true for at least ten years.

Now, there are about €8 million of items on the balance sheet that look like debt at first glance. When I first saw them, I assumed they were loans taken out to finance the Best of TV acquisition.

But they aren’t.

The €5.1 million is a put commitment related to Best of TV. It represents the present value of Passat’s future obligation to buy the remaining 35% of Best of TV from the minority shareholder. So that’s no debt, and it doesn’t compound. In fact, it actually shrinks each year as BOTV pays dividends to that minority holder.

The €2.9M are simply lease liabilities related to capitalized office, warehouse, and car fleet leases.

The real bank debt is zero.

Economically, you have a company with €22 million in cash, no real debt, and about €8 million of operational and accounting liabilities.

What’s really interesting is when we look at current assets relative to total liabilities.

Passat trades at roughly half of net current asset value. A 47% discount, to be exact.

That provides a lot of downside protection. It also means there’s a lot of ground to cover just to get back to liquidation value.

What makes it even more interesting is that the founding family seems to know the stock is cheap.

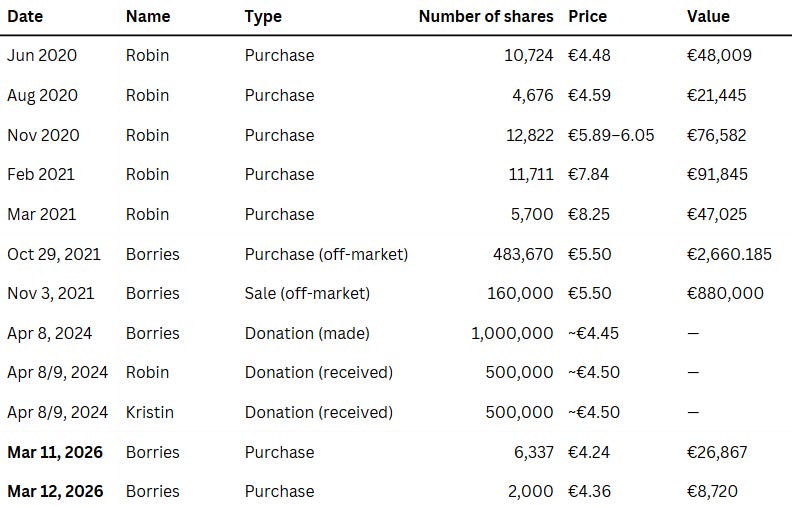

The Insiders Are Buying

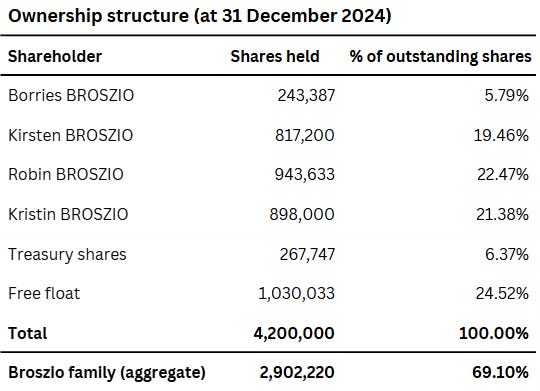

The Broszio family runs this company.

They’re German, based in Hamburg, and collectively own about 69% of the shares and 76% of the voting rights. Borries Broszio, now 81, was CEO for years before handing the role to his son Robin.

Both have been buying shares on the open market.

The March 2026 purchases are the interesting ones.

In April 2024, Borries donated most of his personal shareholding to his two children as part of a family succession plan. His personal stake dropped from over 25% to under 6%.

So when he goes back into the open market in March 2026 and starts buying again, that’s a deliberate choice to rebuild a holding he had largely given away.

The long-run pattern is therefore: the family has repeatedly bought in size when the shares are at or below €5.

Capital Returns

Passat does not have much of a history of returning capital. They do not pay dividends and have no significant history of buybacks.

The first real buybacks happened in 2024. Passat repurchased 21,285 shares at an average price of €4.84.

That’s a signal, taken together with the insider buying, that management thinks the stock is cheap. But it sits in odd contrast to the size of the cash pile.

And the cash pile is not a new development. It has been large for over a decade. It grows, more or less steadily, but most of the time it just sits there on the balance sheet. It earns money-market yields and generates roughly €1 million per year in net interest and investment income, which flatters reported earnings. But it has not been returned to shareholders in any meaningful way.

That is the part that concerns me. Given who controls the company, my fear is that the family treats this cash as a kind of personal savings account.

Valuation

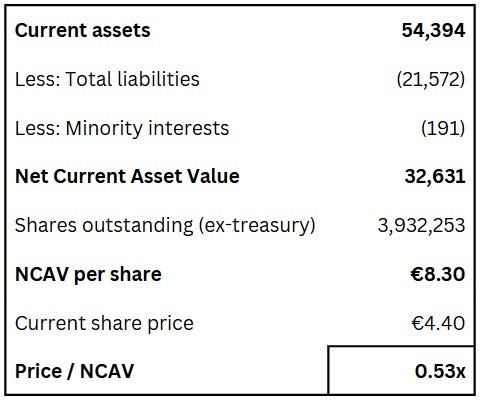

With 3.93 million shares outstanding at €4.40, the market cap is €17.3 million.

The balance sheet carries €22.2 million in cash and marketable securities and zero bank debt. The €8 million of long-term liabilities, as we discussed, are operational and accounting items. Not financial debt in any real sense.

On a straight market-cap-minus-cash basis, the enterprise value is negative. Add back the lease liabilities and the Best of TV put as economic obligations, and the adjusted enterprise value lands at €3.3 million.

That gives you a stock trading at 1.42x EV/EBIT and 0.53x P/NCAV.

Even in a stressed liquidation scenario, the per-share recovery should exceed today’s market price.

The stock also looks cheap on a traditional screen. It has a P/E of about 10, and a price to book of 0.42. But those multiples don’t capture what’s really going on.

Why It’s Cheap

A few reasons come to mind.

First, it’s a small French micro-cap with no English filings. The market cap is €17 million, there is no analyst coverage, and all annual reports come out in French only. You can work with Google Translate and get the broad strokes, but the subtle accounting points probably still get lost.

So the bar to even understanding the business is high relative to the reward, which is a small absolute amount of alpha on a €17M market cap. But hey, alpha is alpha, right?

Second, Passat voluntarily downlisted in October 2025. The company moved from Euronext Paris to Euronext Growth Paris, a less regulated market. The ticker changed from PSAT to ALPAS. This probably saves another hundred thousand euros a year in listing fees and cuts regulatory overhead.

Third, the absence of capital returns. Yes, there have been some small recent buybacks, but relative to the cash position they are pretty much peanuts. And the massive cash pile has grown undistributed for a decade.

Fourth, there’s no real catalyst. The Broszio family controls 76% of the votes, which makes an activist campaign near impossible. The 2024 succession transfer, where the founder passed most of his shares to his two children, signals multi-decade continuity, not an exit event.

The flipside of that is a controlling family with a genuinely long time horizon and a conservative approach to the balance sheet.

Finally, a smaller point but worth mentioning. Most screeners flag the Best of TV put liability as debt. If you don’t go through the actual filings, there is no way to know the company carries zero bank debt.

Risks

The biggest risk is simply that this never moves. The cash pile has been on the balance sheet for a decade, and the family controls most of the votes. So the stock could trade at half of net current asset value forever. If it does, you’ll earn incremental book value from retained earnings, but not much more.

There is also a certain customer concentration, though that also comes with the business model. The top client is 21% of group revenue, the top five are 52%, and the top ten are 71%.

French core erosion also needs to be mentioned. The French standalone entity swung to an operating loss in 2024 and has continued to weaken in 2025. Without Best of TV, the whole group would probably be losing money at the operating level. If the French core keeps slipping, the cash pile will eventually stop growing.

Finally, the Best of TV purchase liability is real money that will eventually leave the balance sheet. Passat is obligated to buy the remaining 35% of Best of TV at some future point. The €5.1 million is already booked as a liability, so it is not a surprise to the numbers, but the cash still goes out the door when the time comes.

Final Thoughts

I spend a lot of time looking for stocks like this.

The honest truth is that I have very little interest in writing about something that already been written up ten times.

Not because I think those ideas are bad, but because being the hundredth person into a stock is just a fundamentally different proposition than being the first.

By the time an idea has made the rounds, the easiest part of the return has usually already happened.

What I am really looking for is the stock that nobody has written about.

This time, that search led me to Passat.

When I did my research, it reminded me of some of Buffett’s early investments. Union Street Railway. Sanborn Maps. Situations where the operating business was secondary and the balance sheet was the whole story.

Passat fits that category. The operating business is small, niche, and stagnating. The family controls the company and is not going to hand the cash back to shareholders on any schedule that suits you.

But the valuation is what makes this a cigar butt worth picking up.

At half of net current asset value and 1.4x EV/EBIT, for a profitable business with a strong balance sheet and insider buying, the downside is well defined. And a correction back toward NCAV is the upside.

Disclaimer: The information provided in this newsletter is intended for informational and educational purposes only. It does not constitute financial, investment, legal, or tax advice. All analyses, opinions, and interpretations reflect my personal views at the time of publication and are provided without reference to the individual circumstances or objectives of any reader. All analyses, information, and opinions have been prepared with great care. Nevertheless, no guarantee can be given as to the accuracy, completeness, or timeliness of the information provided. Use of the content is at the user’s own risk. Investing in securities involves risk, including the possible loss of capital. Readers should conduct their own research and, if necessary, consult a qualified professional before making investment decisions.