A cheap stock hidden on the OTC

And a management team that finally started cleaning up

Key Metrics:

65% of the market cap sits in cash

Management is finally divesting the bad businesses

A hugely profitable, growing core business hiding underneath

A long-term view is its own edge in a short-term market.

As a small private investor, patience is one of the few structural advantages you actually have.

Nobody can force you to sell, and nobody fires you for holding something that does nothing for a year.

Most funds don’t have that luxury.

They are driven by pressure from outside investors, worried about their own careers, and scared to look wrong for six months straight.

That’s what lets patient investors capture the higher returns a long-term view can offer.

And sometimes a long-term view just means being able to look past the current quarterly report.

Vaso Corporation

Ticker: VASO Market cap: $33.26M.

Vaso Corporation is a small company based in Plainview, New York.

It runs three very different businesses inside one corporate shell. All of them pull in opposite directions.

That structure is exactly where the opportunity hides.

So let’s make sure we understand each segment.

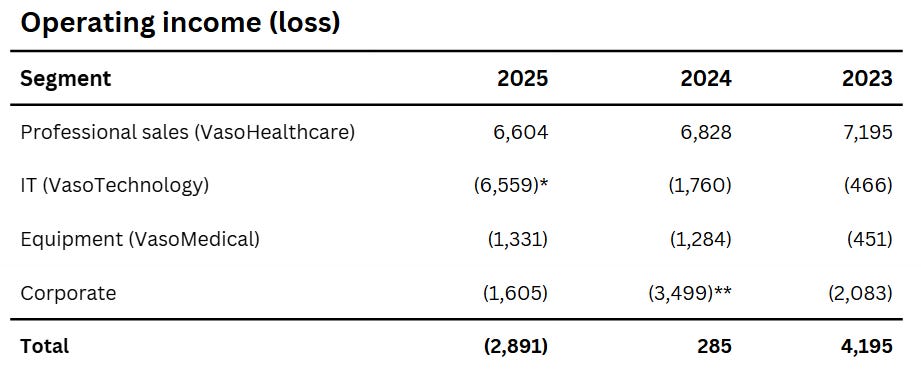

In $ thousands. * Includes a $4,639k goodwill impairment; ($1,920k) without it. ** Includes $1,930k of costs for a failed Achari SPAC deal.

First is the professional sales service segment (VasoHealthcare).

The easiest way to think about this segment is as a commission-based sales agency. Vaso doesn’t own or make anything here, it just sells.

It employs 80-90 salespeople and has been the exclusive outside sales rep for GE HealthCare’s (NASDAQ: GEHC) diagnostic imaging equipment since 2010.

The team sells GE’s MRI, CT, and ultrasound machines to hospitals and clinics across the US. GE delivers the equipment, and Vaso collects a commission.

It’s a very capital light business model.

Second is the IT segment (VasoTechnology).

Until recently this segment had two parts. NetWolves, a managed network and security business Vaso bought in 2015, and VasoHealthcare IT (VHC-IT), a healthcare software reseller (basically a sister business to the professional segment, just for software instead of hardware).

Vaso sold VHC-IT in November 2025, so the IT segment today is essentially just NetWolves, which has been shrinking for years.

The last piece is the equipment segment (VasoMedical).

This is Vaso’s original business, dating back to 1995, and in a way the counterpart to the professional segment. Here Vaso actually designs and builds its own medical devices (mainly EECP systems and Biox devices for cardiovascular therapy and diagnostics), with operations in the US and China.

It’s small, slowly shrinking, and loses money every year.

The professional segment is the crown jewel. That’s worth keeping in mind.

In 2025 it brought in about $44.2 million in commission revenue and it reliably produces $6.6–7 million of operating income, all while being capital-light and growing.

The other two segments together burn ~$2.5–3 million a year before one-off charges, and in doing so they eat up the entire profitability of the good business.

(Hint: that’s the heart of this thesis)

The Numbers From the Outside

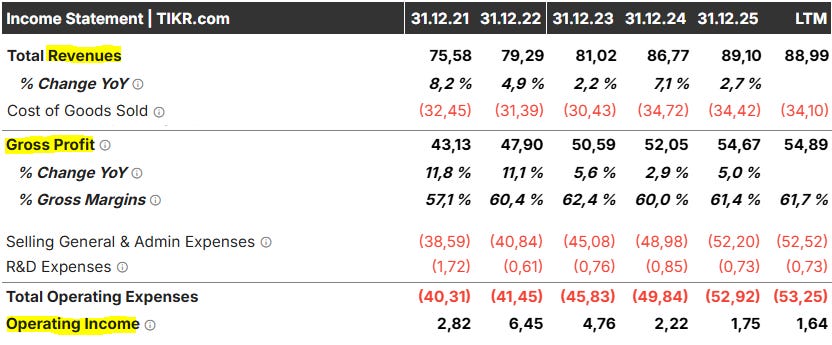

If you just look at the top-line numbers, the situation doesn’t exactly scream opportunity.

Revenue has been growing, but only modestly.

Gross profit climbs along with it. Operating income, though, tells a different story.

The problem comes down to SG&A, which behaves a bit strangely here.

It jumped from $40.8 million in 2022 to $52.2 million in 2025, a 28% increase in three years.

Almost all of the 2025 increase came from the professional sales segment, where SG&A went up by about $3.2 million while the other segments stayed flat.

What exactly is driving that isn’t explained. It definitely has nothing to do with sales commissions paid to employees, those sit in cost of revenues.

The 10-K only says the increase was “attributable mainly to higher sales personnel-related and IT costs.”

What exactly that means is unclear, and I couldn’t get to the bottom of it. That’s something to watch over the next few quarters.

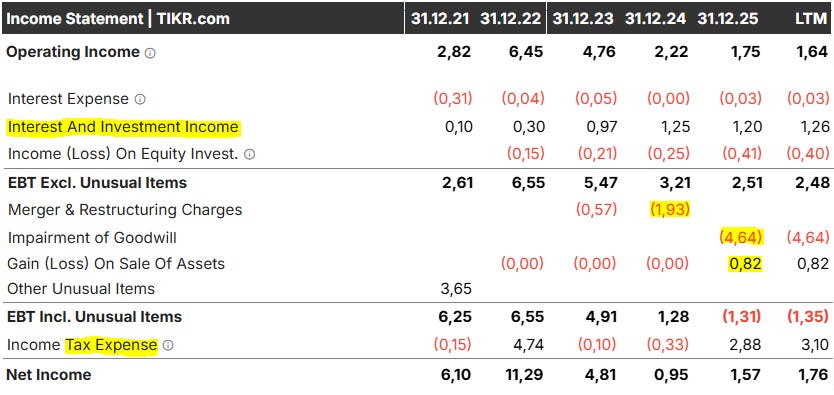

Adjusted for the one-offs in 2024 and 2025 (tikr does that automatically), operating income fell from $2.22 million to $1.75 million, which traces back to the SG&A dynamic above and a growing loss in the equipment segment.

The bottom-line net income, finally, tells you almost nothing.

It gets pushed around by interest income on the cash pile, by tax effects, and by one-offs like the gain on the VHC-IT sale.

Reported EPS of $0.01 and the resulting P/E of 19 are close to useless for valuing this business.

The Balance Sheet

For quite some time, the thesis on this company was simply that it was very cheap on an EV/EBIT basis.

Starting with an exceptionally strong year in 2022, where the professional segment earned $9.5 million of operating income, cushioned by income tax benefits and working capital swings, Vaso built up an enormous cash position. And they kept adding to it.

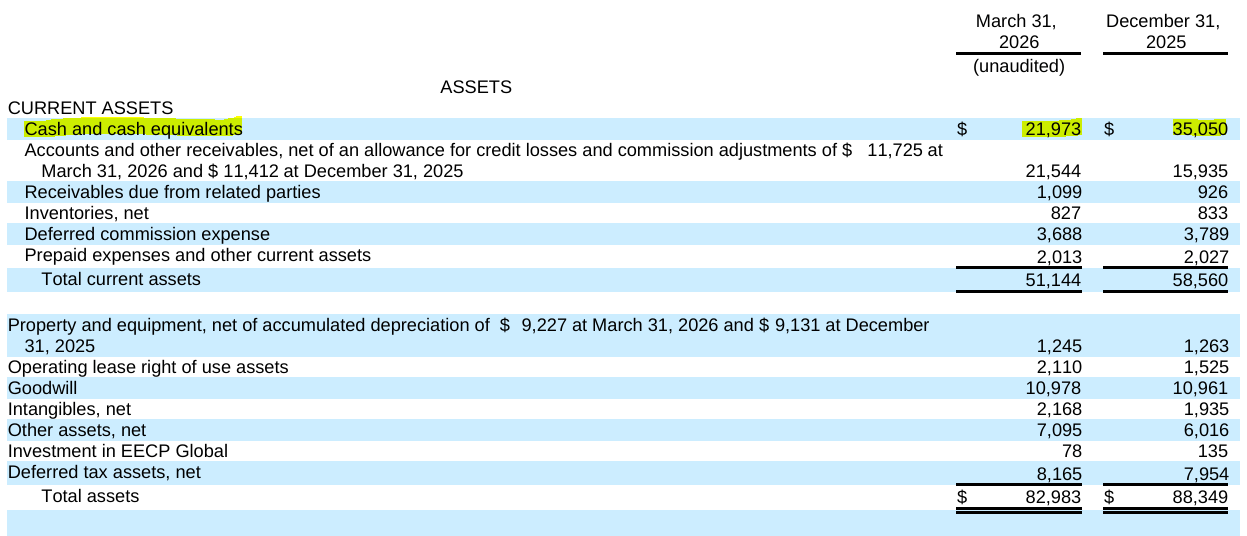

By December 31, 2025, cash had peaked at $35.05 million:

With almost no real liabilities on the books, that cash pile pushed the EV negative against a then ~$30 million market cap.

Some would say you were getting the business for free.

A big driver behind that cash generation is a sort of negative working capital business model.

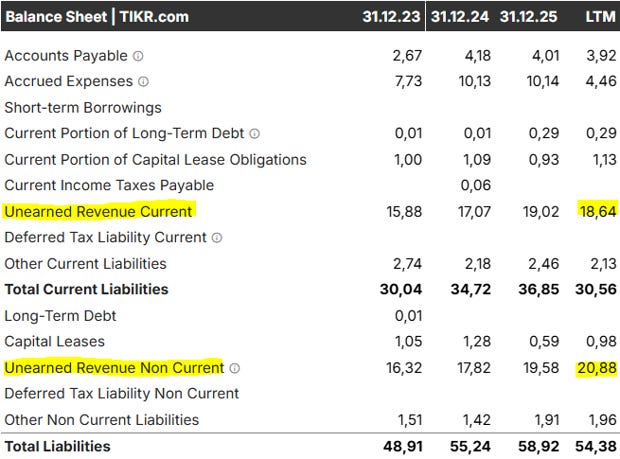

To understand that, it helps to look at two other items on the balance sheet.

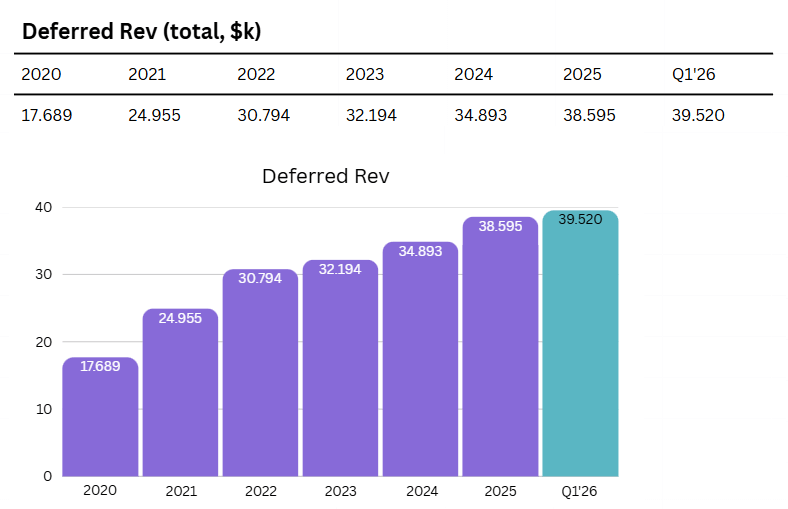

You’ll see $54 million in total liabilities, which sounds like a lot, but about $40 million of that is deferred revenue:

The real liabilities are minimal, just some leases and a small note.

And that deferred revenue comes almost entirely from the professional segment.

The contract balances note in the 10-K describes it like this:

“In our VasoHealthcare business, we bill a portion of commissions on the orders we booked in advance of delivery of the underlying equipment.”

So when a hospital orders GE equipment, Vaso earns a claim to a commission.

Vaso bills part of it, and partly collects it, before GE even delivers the machine. But it can only recognize the revenue once the equipment has been delivered and accepted.

In the meantime, the amount sits on the balance sheet as deferred revenue.

Because Vaso collects part of these commissions up front, a substantial portion of the cash position is float (money held against the deferred revenue.)

That’s exactly why Vaso sits on $35 million of cash despite meager net income.

It’s similar to insurance float, or Costco collecting membership fees before you ever buy anything.

You could, by the way, also look at the deferred revenue as a backlog of booked orders. And that backlog has grown massively. It’s more than doubled since 2020.

Then Came the Q1 Report

On May 15, 2026, Vaso released its latest quarterly report.

If you just glance at it, it looks like the cash position simply dropped by about $13 million. In three months.

Because, well… it frankly did.

Cash went from $35.05 million to $21.97 million:

With the lower cash position, the enterprise value was suddenly no longer negative, and the business no longer “free.”

As of today, July 4, the EV stands at $13.7 million.

And it seems like investors reacted to that news. The share price took quite a hit after the release of the 10-Q and dropped about 25%:

But the surprise here probably wasn’t just that the cash position dropped. For investors who had read the 10-K closely, it was more likely how far it dropped. The 10-K had already disclosed that as of March 27, cash stood at only $29.5 million:

„At December 31, 2025, we had cash and cash equivalents of $35,050,000 and working capital of $21,714,000. At March 27, 2026 the Company’s cash and cash equivalents were approximately $29.5 million.“

That’s quite a bit more than what the quarterly report ended up showing.

It’s Different Than It Seems

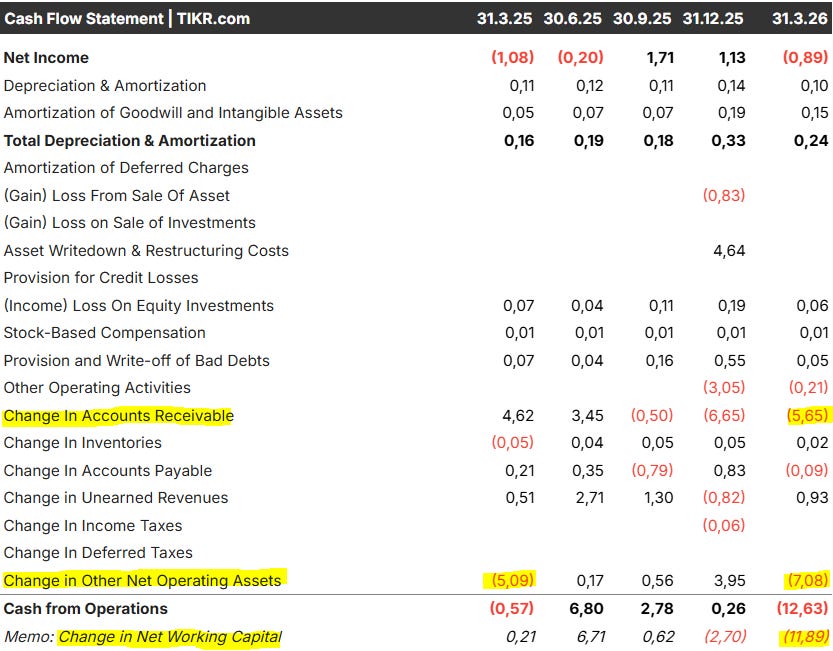

If you take a slightly closer look, you can see it wasn’t as if $13 million simply left the party.

Yes, cash fell from $35.05 million to $21.97 million, but the net loss for the quarter was only $887k.

Almost the entire cash drop came from working capital movements, in other words, timing effects:

The biggest pieces were receivables, which rose by $5.65 million. It looks like a lot of GE equipment was delivered during the quarter, so Vaso recognized the commissions and booked receivables, but hasn’t collected the cash yet.

Total receivables now stand at $21.5 million, and as they get collected over the following quarters, they should turn back into cash.

Accrued commissions and expenses, meanwhile, dropped by about $6 million.

These are the seasonal commissions and bonuses that accrue for the sales force over the year and get paid out in Q1. You can see the same pattern in Q1 2025, and in the years before that.

So the Q1 level of $22 million is very likely a seasonal low, and cash should rebuild toward ~$30 million over the course of 2026 as receivables come in and no big commission payouts are left.

With that, the enterprise value should fall back to ~$3–6 million.

Now Comes the Interesting Part

Remember the three segments from the start?

The professional (GE) segment, the IT segment, and the equipment segment.

I want to highlight something.

How the professional segment has been performing.

Its revenue has climbed sharply over the last several years, almost doubling since 2020, while the IT segment stagnates and equipment slowly drifts down.

Part of that is simply Vaso improving, with higher sales numbers and higher commission rates, but a GE market tailwind plays into it too.

GE HealthCare’s imaging business, the division Vaso sells for, has been growing at mid-single-digit revenue growth over the past years. That’s been masked a bit in their reports by foreign sales, which aren’t relevant for Vaso.

So to some extent, Vaso’s growth is coattail growth. But only to some extent, since the professional segment has been growing faster than the US imaging and ultrasound market.

Either way, those are good coattails to ride.

On the profit level, the contrast between the professional segment and the other segments is even sharper:

* includes the $4,639 goodwill impairment; about (1,920) without it ** includes $1,930 failed-SPAC cost

The professional segment reliably earns $6.6–7 million of operating income, while IT and equipment burn money next to it.

The 10-K makes a point of it too:

“Approximately 50% of our revenue and all of our operating income is generated from sales of GEHC products under this agreement.”

The consolidated numbers you saw earlier, with the unimpressive revenue growth and shrinking operating income, completely bury how good the core business actually is.

A company consisting only of VasoHealthcare, with ~$44 million of commission revenue, ~$6.6 million of operating income, capital-light and growing, plus $30-something million of cash, would be valued completely differently than the current conglomerate look, with a shrinking IT business and a loss-making equipment business wrapped around it.

So naturally, you’d want management to just get rid of the bad segments and let the good one finally show through.

Turns out, they’re already doing it.

Divesting the Bad Businesses

In November 2025, Vaso sold VasoHealthcare IT (VHC-IT), the software-reseller half of the IT segment, to Nano-X Imaging (NASDAQ: NNOX).

The deal itself was small, a roughly $827k book gain and just $200k of cash proceeds.

But forget the numbers.

What actually matters is that management was willing to sell a piece of the business at all.

It’s a first step toward cleaning up the business and giving the professional segment room to show.

(Small side note: in Q1 2026, the first quarter without VHC-IT, the IT segment’s operating loss already narrowed from $798k to $310k year-over-year.)

Still, without a concrete reason to believe they’ll keep improving the business and divesting the bad parts, buying the stock on this thesis alone would be mostly speculation.

If nothing further happens, this could simply become a cheap cash box, that stays at this price for a long time.

But then...

You’ve probably already guessed where this is going.

We got our confirmation.

The 8-K

On May 8, they released an 8-K. It’s short, but it says a lot.

Here’s the whole substance of the filing:

Let’s break this down.

They entered into an agreement with Peter Castle, the President of VasoTechnology (the IT segment.)

Castle can earn $175,000 if he helps Vaso achieve “specified corporate outcomes relating to potential strategic initiatives.” If the objectives are not met, he gets nothing.

A few questions come up: who is Peter Castle, and what “specified corporate outcomes” are we talking about?

Start with Castle, because he’s not just some random segment head.

He was President and CEO of NetWolves itself before Vaso bought it in 2015. He’d been with NetWolves since 1998, and he then served as Vaso’s Chief Operating Officer from 2015 until January 2025.

So he is THE person who knows NetWolves inside and out.

Putting a success-based incentive in front of exactly this person, for “strategic initiatives,” six months after selling the other half of his segment, is already interesting on its own.

But there’s more:

In the 2025 income statement shown earlier, you can see a $4.64 million goodwill impairment that dragged down the year’s results.

That impairment concerned precisely the NetWolves reporting unit inside the IT segment.

Because of the decline the business is going through, its carrying value on the books was higher than what it was actually worth, so Vaso had to write it down.

And even after the impairment, there’s still $9.7 million of goodwill sitting on NetWolves, a shrinking, money-losing business.

So put it together. We have an incentive plan, built around the key person behind NetWolves, the shrinking segment that just took a goodwill impairment and masks the good numbers of the professional segment, announced half a year after the other half of the IT segment was sold.

I’m leaning a bit out the window here, but I’m fairly confident you can read that “specified corporate outcome” as a sale or disposal of the remaining NetWolves business, just wrapped in careful corporate language.

A sale would bring in some cash, sure, but that’s not really the point. I think the bigger benefit is what it does to the income statement.

It clears out the noise and finally lets the GE segment’s $6–7 million of operating income show up on its own, instead of getting swallowed by IT and equipment losses.

And I don’t think the market missed this entirely either.

Right after the 8-K dropped, the stock jumped about 35%, you can see it marked on the chart above.

It’s just that the quarterly report a week later took all the excitement out and pushed the stock right back to where it was.

A nice opportunity.

Normalized Earnings Power

On a look-through basis, the GE segment alone has produced an average of about $6-7 million of operating income over the last three years.

Against a normalized enterprise value of only a few million dollars ($3–6 million once the cash rebuilds), that’s an EV/EBIT of around 1x or less for a stable, capital-light, contracted business.

Even against today’s un-normalized EV of ~$13.7 million, you’re paying about 2x.

However you slice it, this is cheap. The only reason it doesn’t look that way is the losses sitting around the professional segment, dragging the whole picture down.

Risks

GE concentration is the big one. The entire crown jewel hangs on one contract.

The original agreement was a three-year deal ending in 2013. It has been extended many times since. In December 2025, Vaso extended the GE agreement by another four years, through December 31, 2030.

So as of today, the good business has a clear contracted life through the end of the decade.

But there’s no guarantee it won’t be terminated early. If GE ends this contract, or worsens the terms, the whole thesis collapses.

Also worth noting, on the GE side, their imaging segment reported margin pressure in 2025. Segment EBIT fell by $71 million, driven by cost inflation, including new tariffs.

That’s not directly Vaso’s problem, but it’s not irrelevant either. If it pushes GEHC to raise equipment prices, hospital demand could soften, and Vaso would feel that pain secondhand.

Then there’s insider control. Vaso is firmly insider-controlled. Joshua Markowitz holds about 31.9% of the stock, and directors and officers as a group hold 43.85%. The company has never paid a dividend and states plainly that it doesn’t intend to.

There was one attempt at a liquidity event, the Achari SPAC, but that deal fell apart.

This is exactly why the clean-up activity, and the Castle incentive, matter.

They turn the thesis from just “it’s cheap” into “it’s cheap, and management is finally doing something.”

The failed Achari SPAC deal showed that this management thinks about strategic transactions and possible exits. The VHC-IT sale showed they’ll actually pull the trigger on a disposal.

Final Thoughts

I think Vaso is a perfect example of something that screens badly.

You have a good business overshadowed by bad ones. The profitability and growth of that good segment only becomes visible once you go into the filings and look at the actual numbers.

That’s probably a big part of why this opportunity exists in the first place.

A business consisting only of the professional segment would very likely be valued completely differently.

That’s exactly what makes the recent moves so interesting, the VHC-IT sale, and now the 8-K. They’re a step toward cleaning up this business and giving the professional segment room to finally show what it’s worth.

One last thing: the idea that NetWolves is being disposed of is my interpretation, not a confirmed fact. Nowhere do the filings say “we are selling NetWolves.” I could be wrong.

I hope you enjoyed this writeup.

Best,

Noel.

PS: I can’t take full credit for this discovery. A friend flagged this 8-K to me, I would have probably missed it otherwise. Thanks, Mike.

Disclaimer: The information provided in this newsletter is intended for informational and educational purposes only. It does not constitute financial, investment, legal, or tax advice. All analyses, opinions, and interpretations reflect my personal views at the time of publication and are provided without reference to the individual circumstances or objectives of any reader. All analyses, information, and opinions have been prepared with great care. Nevertheless, no guarantee can be given as to the accuracy, completeness, or timeliness of the information provided. Use of the content is at the user’s own risk. Investing in securities involves risk, including the possible loss of capital. Readers should conduct their own research and, if necessary, consult a qualified professional before making investment decisions.