10 Cheap Stocks Nobody Is Looking At

Small, obscure, and trading far below fair value

Below a $250 million market cap.

That’s where you’ll find most inefficiencies.

Smaller stocks are simply more likely to be mispriced. Both to the upside and the downside. Mainly because fewer eyes are watching them.

Large institutions can’t buy them. Not because they don’t want to. But because they can’t.

In 2024, the average actively managed American equity mutual fund had $2.5 billion in assets under management. (p. 88)

Managing that kind of money creates real constraints. Fund managers can’t own hundreds of tiny positions. Most hold fewer than 100 stocks, with an average position size of $25 million.

Fund rules typically restrict ownership to less than 10% of a company’s voting shares. So a $25 million position means you’re buying companies with market caps of $250 million or larger.

Given the knowledge and skill of many professional money managers (and I mean that seriously), true mispricings are almost never found above that threshold. Except perhaps during periods of broad panic.

Here’s the thing, though.

Individual investors don’t have that problem.

You can put $50,000 into a $30 million company and nobody bats an eye. The edge is right there.

So why don’t more people use it?

Joel Greenblatt nailed part of the answer in You Can Be a Stock Market Genius:

“If you spend your energies looking for and analyzing situations not closely followed by other informed investors, your chance of finding bargains greatly increases.”

Most people just don’t want to do the work. And the ones who might, often talk themselves out of it for social reasons.

Think about it.

Telling someone at a dinner party that you own shares in an $18 million manufacturer nobody’s ever heard of doesn’t exactly generate excitement.

Talking about Nvidia does.

There’s comfort in owning what everyone else owns. It feels safe. Defensible.

But the crowd doesn’t hand you bargains. The crowd is where you pay full price.

Now, I like to look where the crowd isn’t.

I like to spend my evenings scrolling through obscure listings, OTC tickers, and the smallest names my screeners can find.

It’s not glamorous. But you find things.

Some companies I discard immediately. Others I look at more closely. A few land on my watchlist. And occasionally, one turns into a full write-up.

Over time, I’ve built up quite a collection of tiny, cheap, and ignored businesses.

Many of them were just a little too small, too illiquid, or too inconsistent in their reporting to deserve a standalone article. But that doesn’t make them uninteresting.

I went back through that list recently and pulled out the ten names I find most compelling right now, businesses I’ve never written about before.

Among them, you’ll find four trading below 5x earnings, five below NCAV, heavy buybacks, strong book value growth, balance sheet cleanups, and immense cash positions.

Let’s take a look.

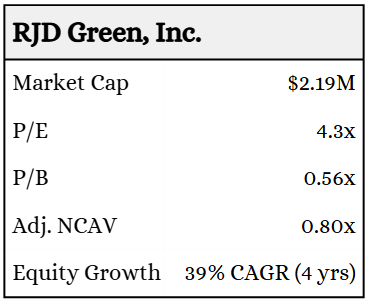

RJD Green, Inc.

RJD Green is about as small as it gets. We’re talking a $2.2M market cap, 4.3x LTM earnings, and 0.56x book value.

The company operates as a holding company with three parts: a specialty construction unit, a healthcare software division, and an environmental segment.

The core business is Silex Holdings, which manufactures and installs countertops, cabinets, and related products for residential and commercial construction markets. It runs fabrication and distribution out of Oklahoma and serves builders, contractors, and remodelers.

It’s an unusual setup, but the business itself is real and growing. Revenue reached $6.86M in fiscal 2025, up from $5.72M the year before.

Net income came in at $480k, which was lower than the $894k earned the prior year, but earnings here tend to move around depending on project timing. The profitability track record over recent years is consistent.

It’s cheap on earnings, but the balance sheet makes it even more interesting.

Shareholders’ equity has grown at a 39% CAGR over the past four years. The company holds $1.3M in cash, carries little debt, and trades below NCAV plus investments.

Now, the risks.

Construction is cyclical by nature, large contracts can distort reported results, and management has historically gone after acquisitions, which brings a whole other set of things to think about. The share count is also quite large, which isn’t ideal, and disclosure quality is limited.

But at the end of the day, this is a profitable operating business trading at deep asset value with meaningful cash relative to its size.

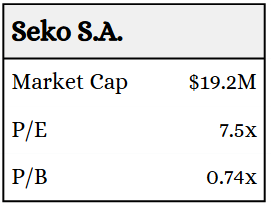

Seko S.A.

Seko is a Polish food producer.

Marinated fish, ready meals, salads, smoked seafood, more than 200 product variations distributed through retail chains, private-label programs, and export markets.

Not the most glamorous business in the world, but that’s kind of the point.

At a $19M market cap, the stock trades at 7.5x earnings and 0.74x book value. Add in consistent profitability, a long operating history, and no share dilution whatsoever, and you’ve got something that’s hard to dismiss.

Fish processing isn’t exciting. But it produces repeat demand, and Seko has built a product range flexible enough to serve both branded and private-label customers.

Recent financials show steady performance. Revenue has grown at roughly 5.3% annually over the past decade and was up year over year through the first nine months of 2025.

The balance sheet is solid too. Equity is growing, long-term debt is declining, and financial investments that support operations add to net income.

The business is family-influenced, with a clear long-term orientation. In late 2025, Tomasz Kustra was appointed CEO, continuing leadership continuity within the founding family.

Honestly, there isn’t much to complain about here. The growth won’t blow anyone away, but it doesn’t need to at this valuation.

My only real hesitation is a personal one. Poland just isn’t where I tend to focus my research. Plenty of smart investors do, and I understand why.

A durable consumer staples business with consistent profitability, a clean balance sheet, and a cheap price tag is a perfectly reasonable thing to own.

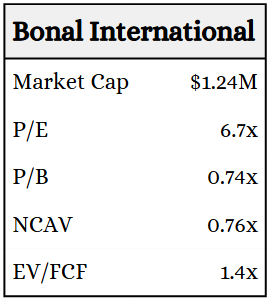

Bonal International, Inc.

Bonal International is exactly the kind of business I’m usually looking for. Cheap, tiny, and easy to overlook.

I really like it. The only real knock against it is simply that it’s very small.

The company sells and rents equipment that uses sub-harmonic vibration to relieve residual stress in metal parts.

Here’s the idea: when you form or weld a metal part, internal stress builds up inside the material. The traditional fix is heat treatment, where you essentially bake the stress out. Bonal’s equipment does the same thing with controlled vibration instead. I had never heard of this before I looked it up.

Bonal also sells related services like training, consulting, and stress relief work, and markets three product lines: Meta-Lax Stress Relief, Pulse Puddle Arc Welding, and Black Magic.

The business is small but real. Fiscal 2025 revenue came in at $1.74M, gross profit at $1.33M, and net income at $143k, which is the best result the company has posted in four years.

Gross margins are high, profitability has been consistent, and the balance sheet looks clean for something this size.

Cash stands at $1.06M against total liabilities of just $313k, mostly current items and lease obligations, with no long-term debt.

The stock trades at 76% of NCAV.

There are a couple of things worth watching. Four customers accounted for roughly 75% of receivables at year end. That’s a real concentration risk. And the financials are reviewed, not audited. That’s not unusual for a microcap like this, but it’s something to keep in mind before sizing up.